Fieldwork conducted on 5 – 8 May

2026

According to BRC-Opinium data, consumer expectations

over the next three months of:

-

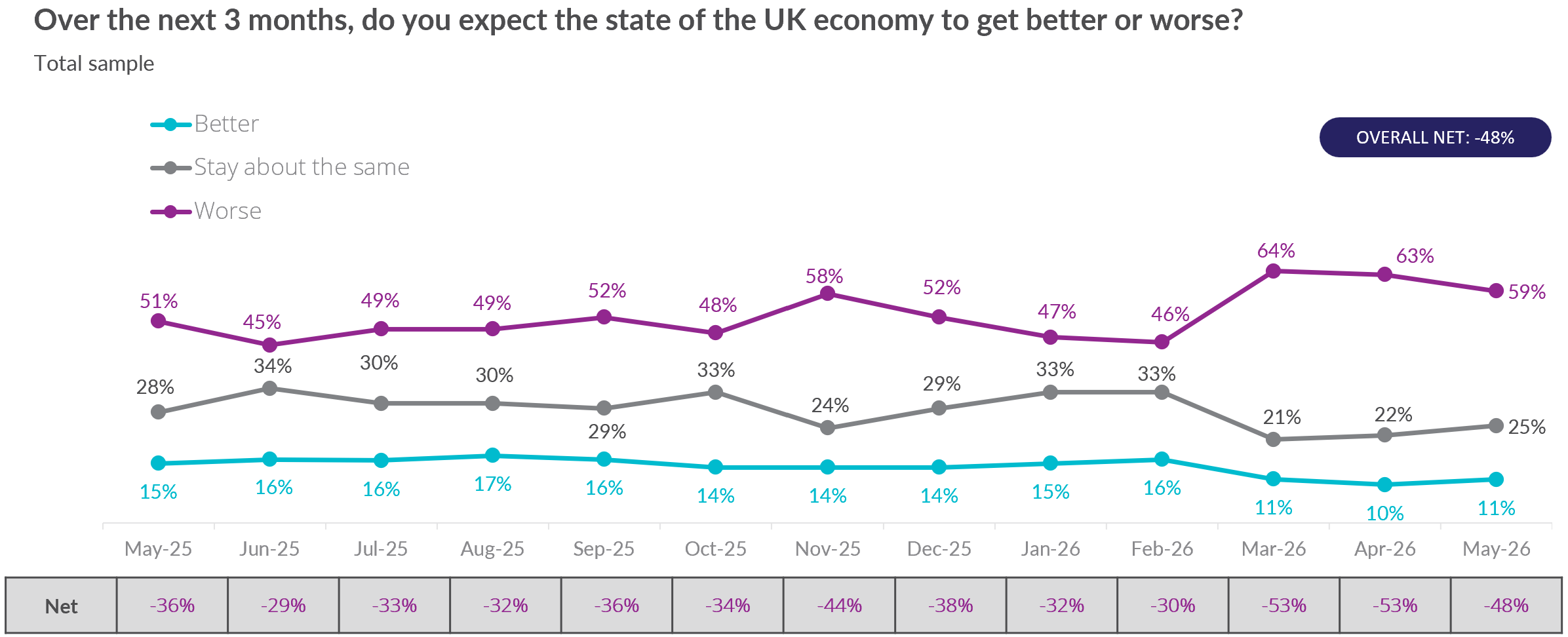

The state of the economy improved at -48 in

May, up from -53 in April.

-

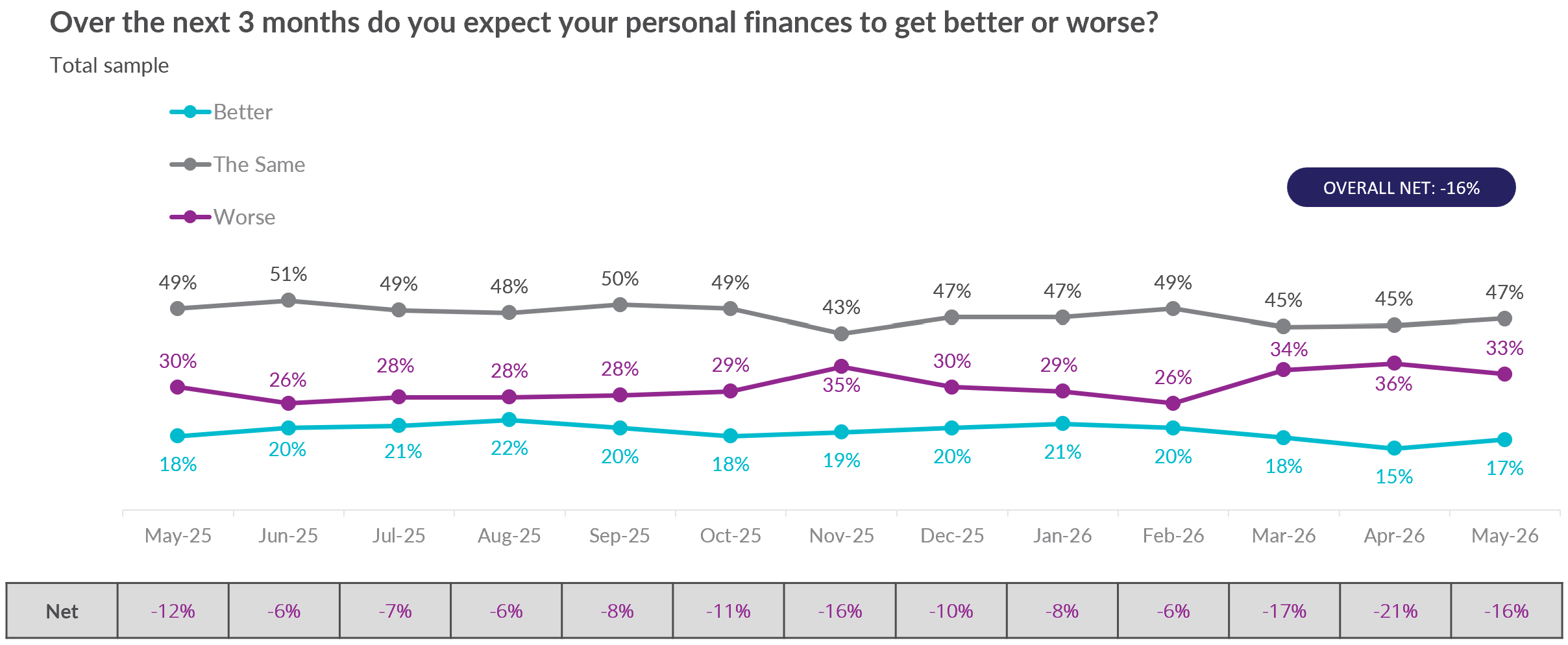

Their personal financial situation improved to

-16 in May, up from -21 in April.

-

Their personal spending on retail rose to +7

in May, up from +5 in April.

-

Their personal spending overall remained at

+15 in May, the same as in April.

-

Their personal saving remained at -8 in May,

the same as in April.

The proportion of people concerned that conflict in the

Middle East could…

-

Increase the price of food rose to 82% in May,

up from 80% in April.

-

Increase the price of non-food rose to 74% in

May, up from 73% in April.

-

Increase energy bills rose to 83% in May, up

from 81% in April.

Helen Dickinson, Chief Executive of the British Retail

Consortium, said:

“Consumer confidence, while firmly negative, saw a slight lift in

May following signs of de-escalation in the Middle East. Younger

consumers drove this improvement in expectations for the economy

and household finances, helped by rising real wages among this

generation. But the outlook remains fragile: inflation is set to

rise, and more than four in five people expect food prices to

climb.”

“If Government wants to keep consumer confidence heading in the

right direction, it must now make a choice: act now, or let these

inflationary pressures spiral, pushing up prices for households.

Energy prices are pushing up costs for retailers and their supply

chains, with the government's energy taxes and levies making up

as much as 65% of business bills. Cutting these charges is the

fastest way to ease inflation and support consumer confidence.

Delay will only make the next cost of living squeeze harder for

households.”

Consumer expectations for the state of the economy

over the next three months:

Consumer expectations for their personal financial

situation over the next three months:

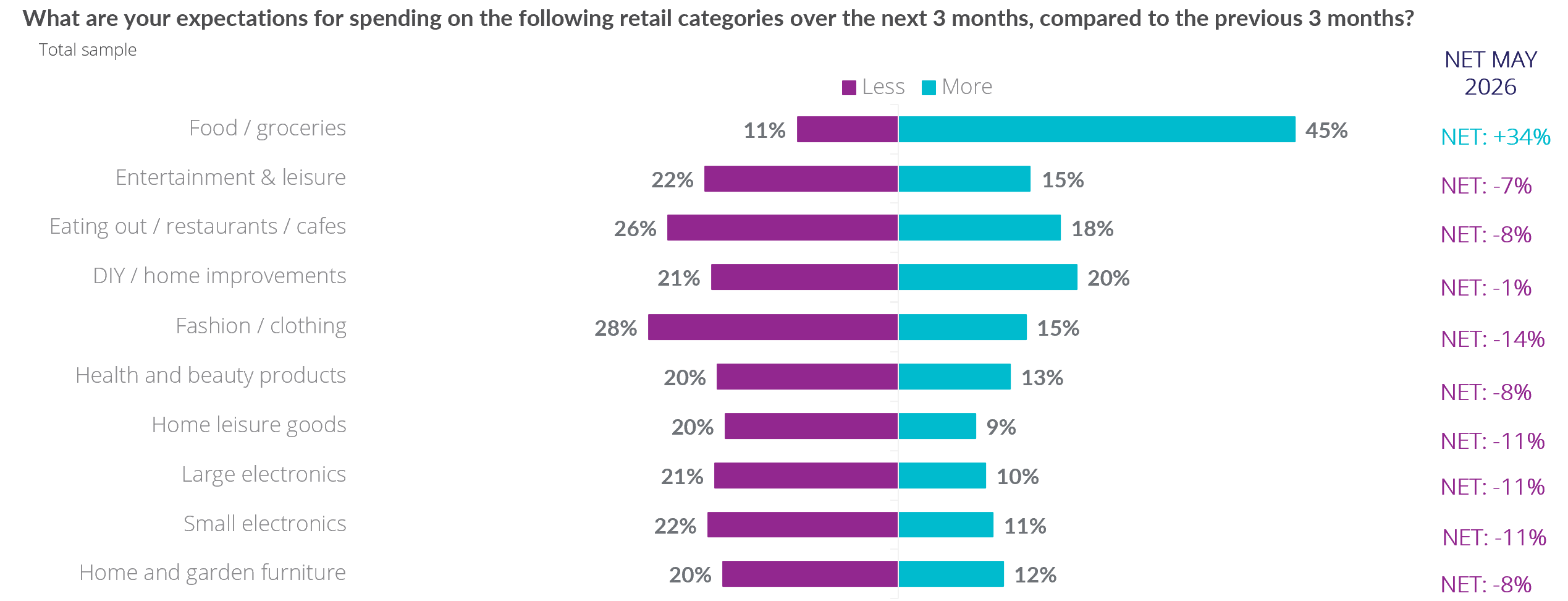

Consumer expectations of spending over the next three

months by category:

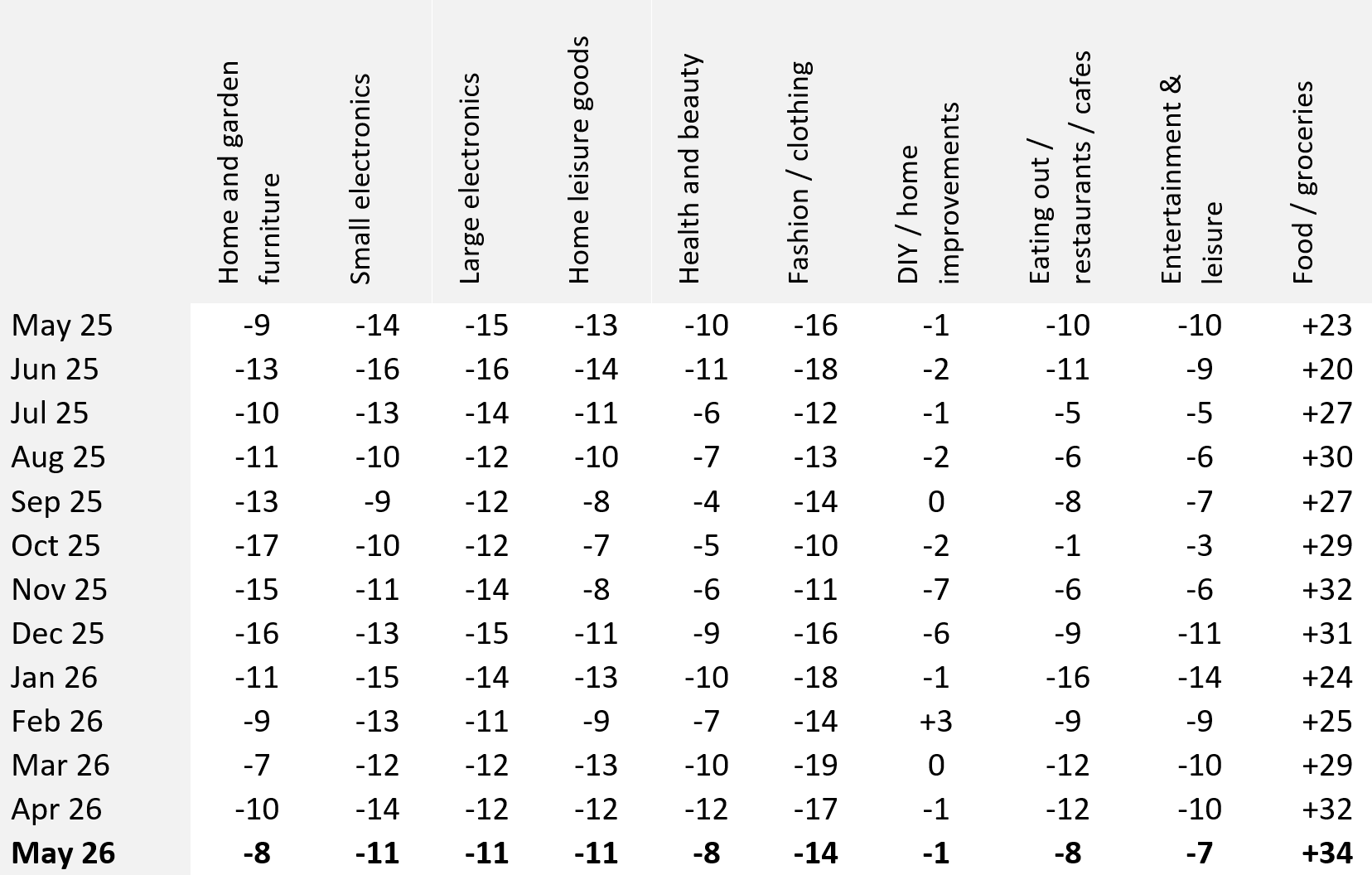

Consumer NET expectations of spending over the next

three months by category:

-ENDS-

Data collection began in March 2024 – and all records are since

then.

The BRC sent this release to our "Monitors" and "General

Retail" media list. To check/update what media lists you are on,

please contact us below.

Methodology:

Fieldwork conducted by Opinium for the BRC. Sample included 2,000

UK adults and results have been weighted and assigned a net

score. The better/worse figures in the graphs are rounded, while

net scores are calculated from precise figures. Questions were:

- Over the next 3 months, do you expect your personal finances

to get better or worse?

- Over the next 3 months, do you expect the state of the UK

economy to get better or worse?

- What do you plan to do in relation to your spending over the

next 3 months?

- Reflecting on your retail spend across different categories,

overall do you expect to spend more or less on retail items over

the next 3 months?

- What are your expectations for saving over the next 3 months?

- What are your expectations for spending on the following

retail categories over the next three months compared to the

previous 3 months?

If you would like the results of the questions by Gender,

Generation, Location, Working status, or Income, please contact

the Press Office. Generations are defined as: Gen Z (18-29),

Millennial (30-45), Gen X (46-61), Boomer (62-80).

This monitor was started in March 2024, and records are from this

date.