Covering the 4 weeks of 1 – 28 February 2026

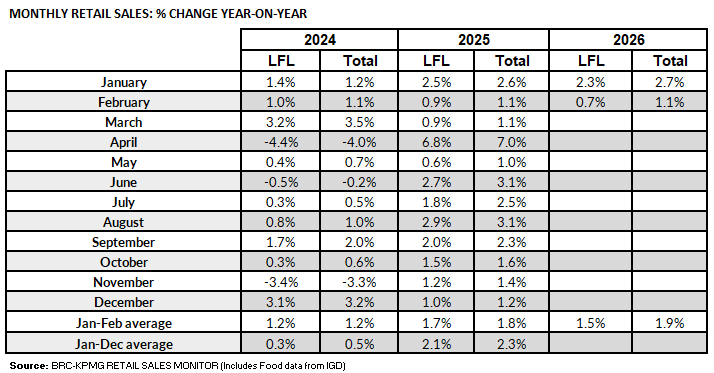

- UK Total retail sales increased by 1.1% year on year in

February, against a growth of 1.1% in February 2025. This was

below the 12-month average growth of 2.3%.

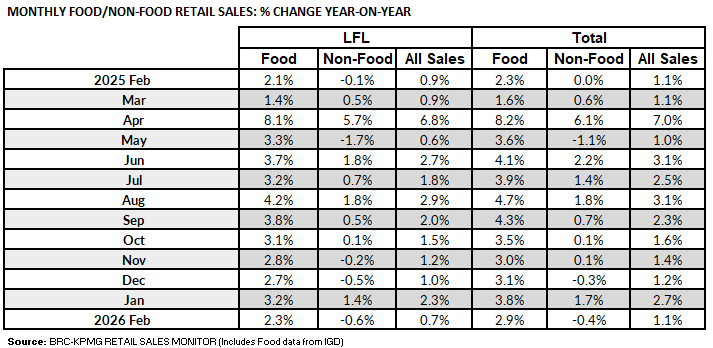

- Food sales increased by 2.9% year on year in February,

against a growth of 2.3% in February 2025. This was below the

12-month average growth of 3.8%.

- Non-Food sales decreased by 0.4% year on year in February,

against 0.0% in February 2025. This was below the 12-month

average growth of 1.0%.

- In-Store Non-Food sales increased by 0.2% year on year in

February, against a decline of 1.0% in February 2025. This was

below the 12-month average growth of 1.0%.

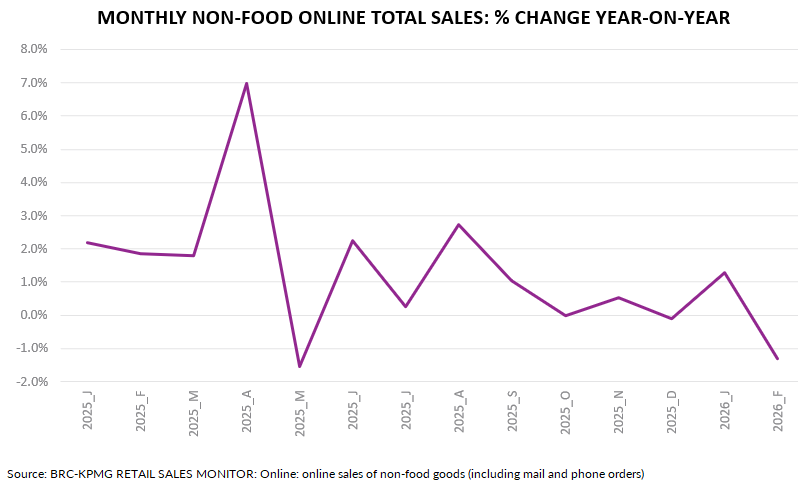

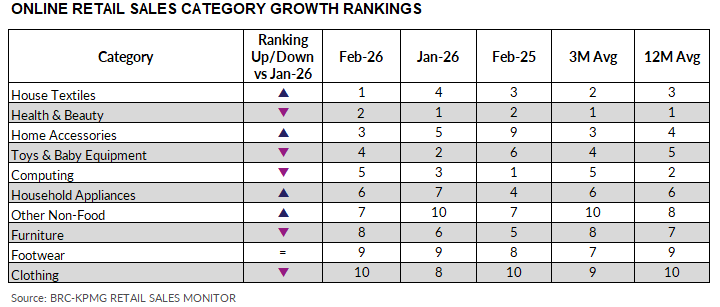

- Online Non-Food sales decreased by 1.3% year on year in

February, against a growth of 1.9% in February 2025. This was

below the 12-month average growth of 1.2%.

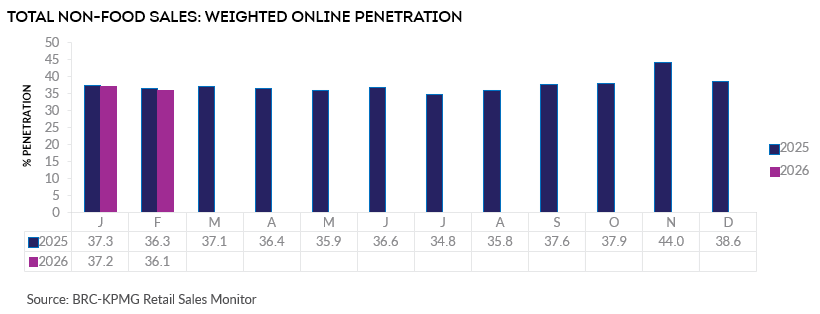

- The online penetration rate (the proportion of Non-Food items

bought online) decreased to 36.1% in February from 36.3% in

February 2025. This was below the 12-month average of 37.3%.

Helen Dickinson, Chief Executive at the British Retail

Consortium, said:

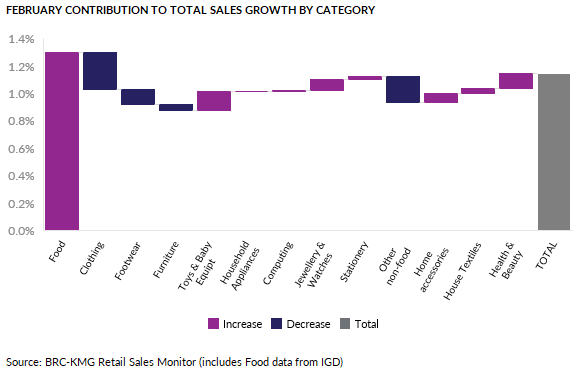

"February's grey, wet weather hit retail sales hard. Spending was

weak across most categories, online and instore, as households

pulled back after Christmas and January's rebound. Food sales

were flat in real terms as shoppers tightened their belts.

Valentine's Day did provide a bright spot, with jewellery,

watches and perfume performing better as people still treated

loved ones.

"While retailers look to Spring and better weather to lift

spirits and revive sales, conflict in the Middle East threatens

knocking any recovery off course. Prolonged low consumer

confidence adds strain on retailers already facing mounting cost

pressures, higher taxes and a growing regulatory burden. At such

a time, government's top priority should be to avoid piling on

further cost and complexity and to think carefully about the real

world impacts of aspects of the Employment Rights Act. Without

realism and restraint, retailers will struggle to invest in the

jobs the economy needs and prices households can afford."

Linda Ellett, UK Head of Consumer, Retail & Leisure,

KPMG, said:

“Health and wellbeing related purchases helped to drive modest

monthly retail sales growth in February. But minus food and drink

sales, the momentum wasn't strong enough to keep growth going for

total non-food goods.

“While some channels, categories, and brands are showing there is

still room to thrive, the combination of ongoing business costs

and limited consumer spending is challenging others – with

efficiency drives and technological transformation continuing at

pace.”

Food & Drink sector performance | Sarah Bradbury,

CEO, IGD, said:

“February delivered one of the wettest months on record, yet

shopper sentiment still saw a modest lift thanks to easing

inflation and news of a forthcoming 7% cut in energy prices,

offering a rare sense of financial reprieve. Seasonal spikes

around Valentine's Day and Pancake Day boosted at home dining but

failed to translate into volume growth. As March begins, the

outlook is deteriorating. The OBR's latest forecast downgraded

near term growth, whilst the conflict in the Middle East is

strengthening concerns over fuel costs, which could impact food

price inflation, if the situation continues. Together, these

risks suggest February's uptick in sentiment may prove short

lived.”