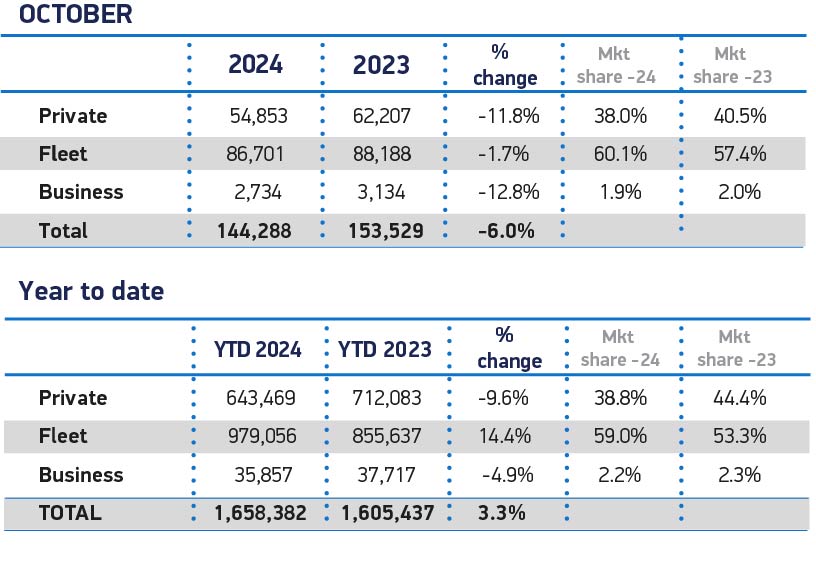

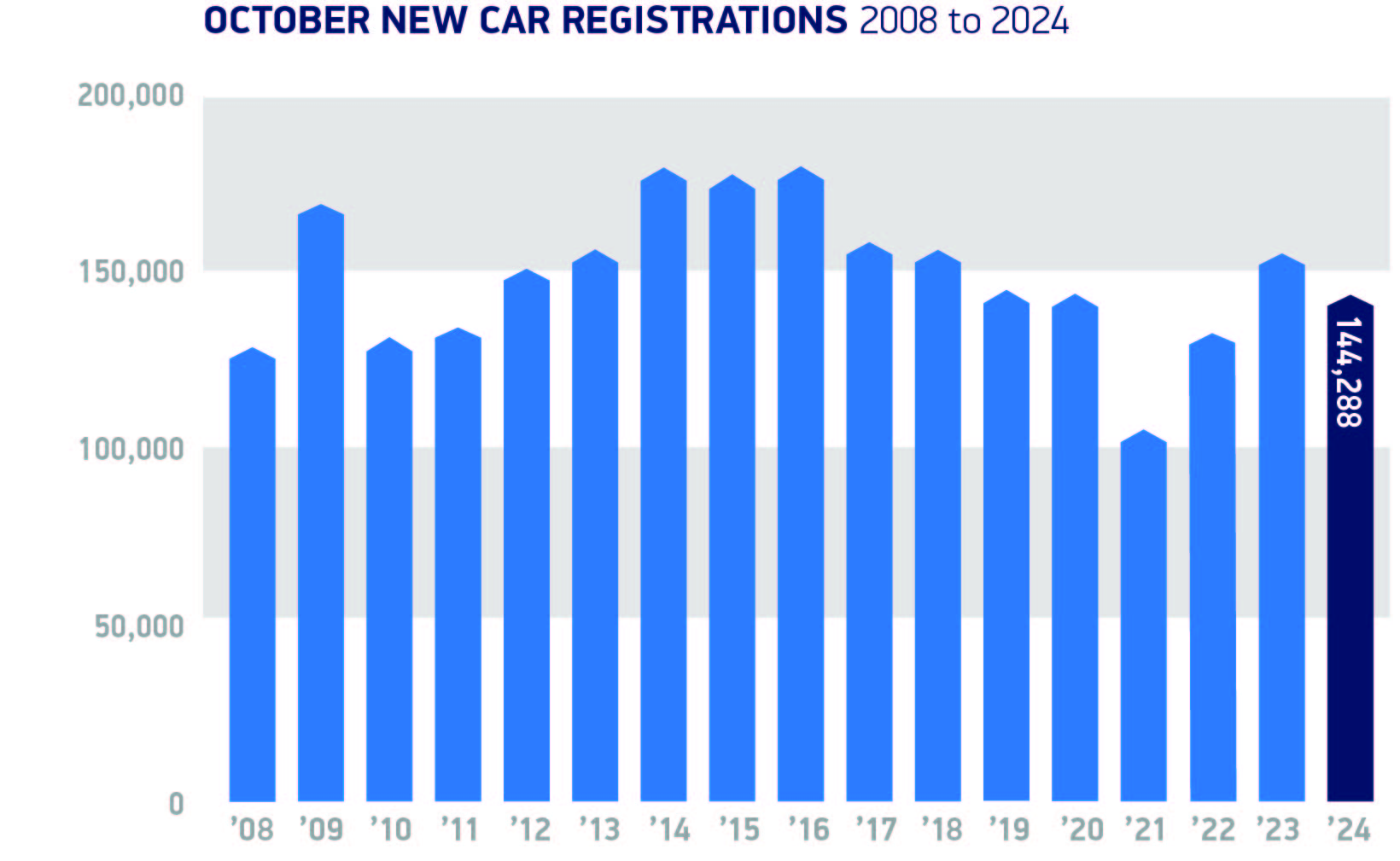

The UK new car market fell for the second time this year, down by

-6.0% in October to 144,288 new registrations, according to the

latest figures from the Society of Motor Manufacturers and

Traders (SMMT).

Declines were recorded across all buyer types, with fleets

falling for the second time this year, down -1.7%, and the

low-volume business market declining -12.8%. Private purchases

continued their two-year long wane, down -11.8% meaning fewer

than four in 10 (38.8%) of new cars registered in the first 10

months have gone directly to private buyers.

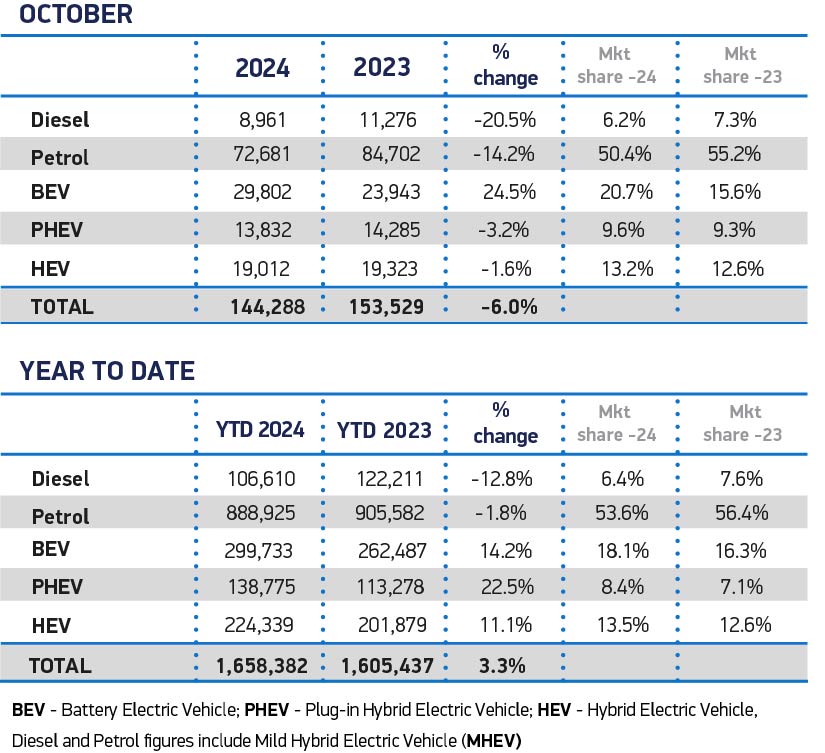

The fall was driven by double-digit drops in petrol and diesel

vehicle deliveries, down -14.2% and -20.5% respectively. However,

uptake of hybrid electric vehicles and plug-in hybrid electric

vehicles also fell, down -1.6% and -3.2%. Battery electric

vehicles (BEVs) were the only powertrain to record growth, with a

raft of new models driving the strongest growth this year, up

24.5% to reach a 20.7% share of the market.

UK new car buyers now have more than 125 different BEV models to

choose from – an uplift of 38% over the last 10

months.1 While it remains the case that the average

BEV has a higher upfront cost than an ICE equivalent, widening

choice and huge manufacturer discounting mean that around one in

five BEV models now has a lower purchase price than the average

petrol or diesel car, especially for buyers able to take

advantage of schemes such as salary sacrifice.2

However, while BEV market share is increasing, October's decline

in the total market, equivalent to a £350 million loss in

turnover, highlights the challenge ahead.3 While

almost 300,000 new BEVs have reached the road in 2024, this

represents 18.1% of the market – an increase on 2023, but still

significantly short of the 22% target for this year and of the

28% which must be achieved in 2025 under the Vehicle Emissions

Trading Scheme.

While the Budget extended existing business and fleet incentives

for BEVs, the Vehicle Excise Duty and Company Car Tax changes

disincentivise low carbon vehicle purchases and fleet renewal

generally, risking a delay to the overall reduction in road

transport emissions.

Moving the market rapidly towards these ambitious targets needs

bold and compelling incentives for consumers. Manufacturers are

currently shoring up demand with historic levels of support, but

this is unsustainable in the long term as it threatens viability.

Without the government support to match the manufacturers'

commitment, there must be an urgent review of the market's

performance and the regulatory mechanisms driving the transition.

Mike Hawes, SMMT Chief Executive, said,

“Massive manufacturer investment in model choice and market

support is helping make the UK the second largest EV market in

Europe. That transition, however, must not perversely slow down

the reduction of carbon emissions from road transport. Fleet

renewal across the market remains the quickest way to

decarbonise, so diminishing overall uptake is not good news

for the economy, for investment or for the environment. EVs

already work for many people and businesses, but to shift the

entire market at the pace demanded requires significant

intervention on incentives, infrastructure and regulation.”

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Notes to editors

With the Budget delivered on 30 October, publication of

SMMT's latest market outlook will be deferred until later

in November, to ensure any potential impacts are

appropriately incorporated.

1 Based on battery electric vehicle models receiving

their first registration between January and October 2024

2 Based on an average ICE vehicle cost according to JATO

of £30,600, and average costs of models listed for retail

3 Based on the fall in registrations against the average

JATO cost for all cars

|