Covering the five weeks 25 February – 30 March

2024

-

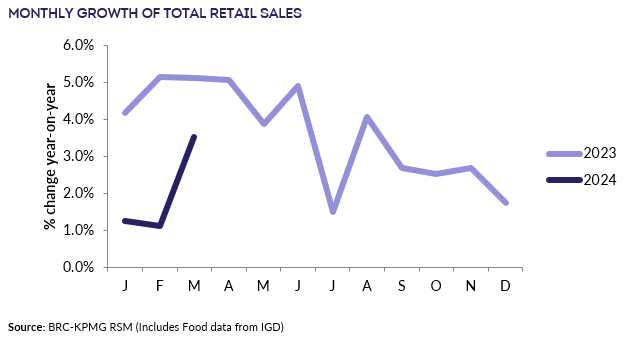

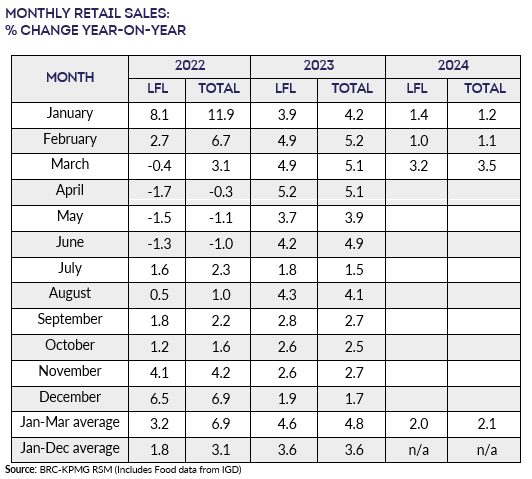

UK Total retail sales

increased by 3.5% year on year in March, against a growth of

5.1% in March 2023. This was above the 3-month average growth

of 2.1% and the 12-month average growth of 2.9%.

-

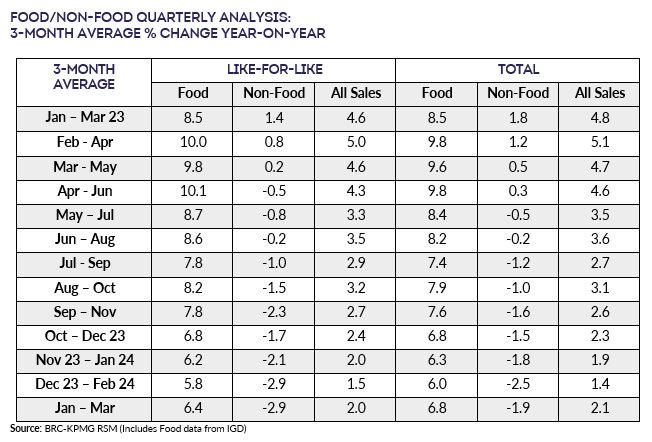

Food sales increased 6.8% year on year over

the three months to March, against a growth of 8.5% in March

2023. This is below the 12-month average growth of 7.7%. For

the month of March, Food was in growth year-on-year.

-

Non-Food sales decreased 1.9% year on year

over the three-months to March, against a growth of 1.8% in

March 2023. This is steeper than the 12-month average decline

of 1.1%. For the month of March, Non-Food was in decline

year-on-year.

-

In-store Non-Food sales over the three months

to March decreased 1.1% year on year, against a growth of 5.2%

in March 2023. This is below the 12-month average of 0.0%.

-

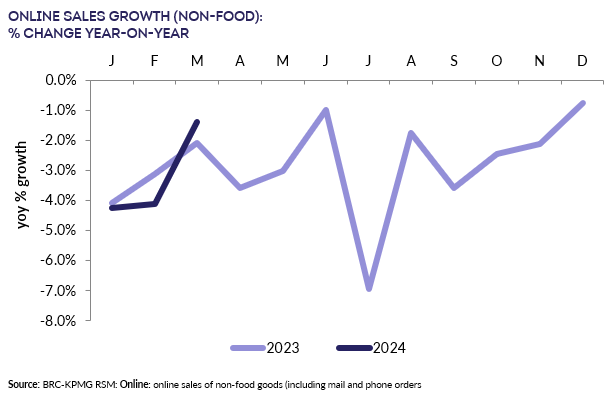

Online Non-Food sales decreased by 1.4% year

on year in March, against a decline of 2.1% in March 2023. This

was shallower than the 3-month and 12-month declines of 3.1%

and 2.8% respectively.

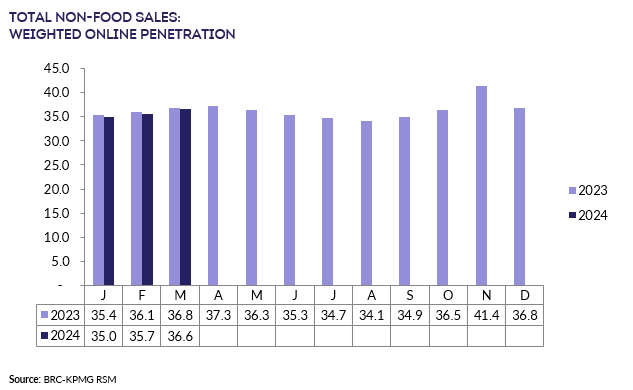

- The online penetration rate (the proportion of Non-Food items

bought online) decreased to 36.6% in March from 36.8% in March

2023. This was higher than the 12-month average of 36.2%.

Helen Dickinson OBE, Chief Executive

of the British Retail Consortium, said:

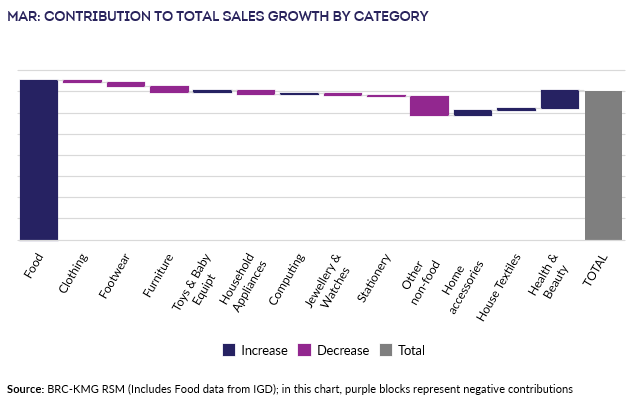

“While retail sales growth improved last month, this was largely

driven by Easter falling unusually early and the subsequent

uplift to food sales in the week preceding the long weekend.

Easter also boosted sales of non-food products such as cookware

and tableware, as people readied themselves to host family and

friends. Home textiles such as throws and pillows were also

popular as consumers sought to spruce up their homes ahead of

Spring. Elsewhere, wet weather dampened sales of garden

furniture, BBQs, DIY products, and clothing and footwear.

“After a difficult start to the year, retailers are hopeful that

with warmer weather around the corner, consumer confidence will

spring back up. A strong retail industry can boost investment

across our towns and cities, and as we gear up for a general

election, it is essential the next government recognises this and

rethinks the burdensome costs imposed on retailers. With a

pro-growth policy landscape, retailers can step up their

investment in innovation and in local jobs and communities up and

down the country.”

Linda Ellett, UK Head of Consumer Markets, Leisure &

Retail, KPMG, said:

“An early Easter showed green shoots of spring for retailers in

March, with sales growth up a more positive 3.5% on last year,

and above headline inflation for the first time in more than two

years.

“High street sales growth was driven by food and drink, health

and beauty and keen gardeners who headed outside to enjoy the

first days of spring. There were also some signs of

improvement with more categories starting to see positive sales

growth in March for the first time in months. Online sales,

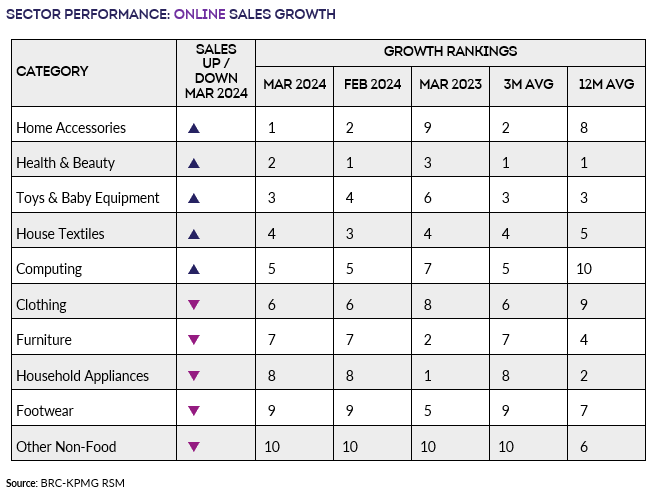

however, continued to slide, falling by 1.4% despite strong

performances in home accessories, health, beauty, and homewares.

“As April signals big increases in the sector's cost base –

through the rise in minimum wage rates and business rate hikes

for the larger high street brands – retailers will be hoping that

the bounce back of March sales is more than just an Easter

blip. Economic indicators are heading in the right

direction with inflationary pressures easing and interest rates

having potentially peaked, however consumer confidence remains

fragile, and households continue to keep a close eye on where

their tight budgets are being spent. It remains a

challenging environment, but as we head into the warmer months,

retailers will be hoping that stronger consumer confidence will

turn into stronger retail sales, especially in more discretionary

categories such as clothing, following an incredibly difficult

few years.”

Food & Drink sector performance | Sarah Bradbury,

CEO, IGD, said:

“The UK grocery market benefitted from Easter falling in March

this year. This has led to very positive comparisons with

spending increasing on March 2023, and importantly significant

volume growth. This marks the fourth consecutive month of

year-on-year volume growth, offering hope to retailers and

suppliers of finally being able to regrow margins that have

shrunk during the cost-of-living crisis.

“Shoppers faced a multitude of financial changes this month from

the anticipation of ‘price hike Monday' to the budget

announcement that cut National Insurance for the second time in

six months. At a total level, shoppers have a growing confidence

in their financial outlook, however the strength of this growth

varies by household income. For lower income households,

confidence is growing at a slower rate despite news of an almost

10% increase to the national living wage. For all shoppers, we

expect the cautious approach to continue as cost-of-living

challenges remain.”