Sales figures are not adjusted for inflation. Given that both the

November SPI (BRC) and October CPI (ONS) show inflation running

at higher than normal levels, the rise in sales masked a likely

drop in volumes once inflation is accounted for. Like-for-like

data has been moved from the bullets to the tables at the bottom.

Covering the four weeks 29 October – 25 November

2023

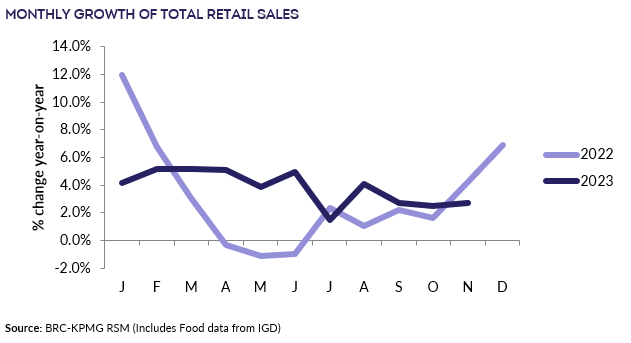

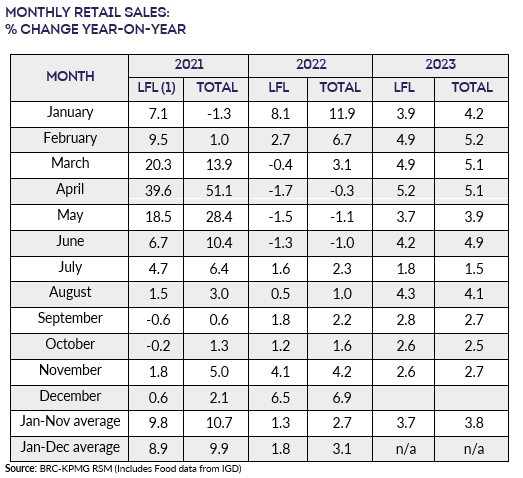

UK Total retail sales increased

2.7% in November, against a growth of 4.2% in November 2022. This

was above the 3-month average growth of 2.6% and below the

12-month average growth of 4.1%.

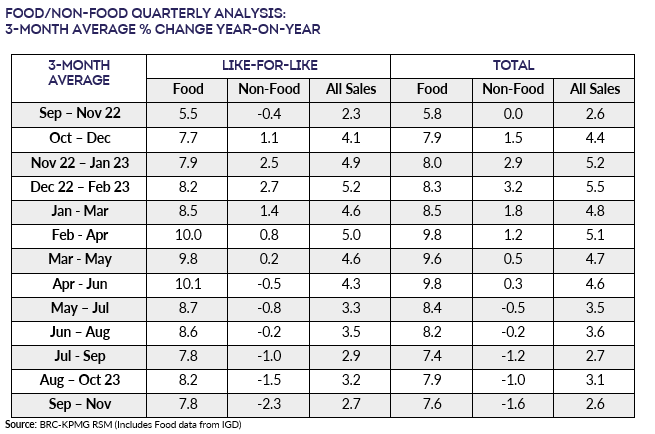

Food sales increased 7.6% on a Total basis over

the three months to November. This is below the 12-month average

growth of 8.4%. For the month of November, Food was in growth

year-on-year.

Non-Food sales decreased 1.6% on a Total basis

over the three-months to November. This is below the 12-month

average growth of 0.5%. For the month of November, Non-Food was

in decline year-on-year.

Over the three months to November, In-store Non-Food

sales decreased 0.8% on a Total basis since November

2022. This is below the 12-month average growth of 0.6%.

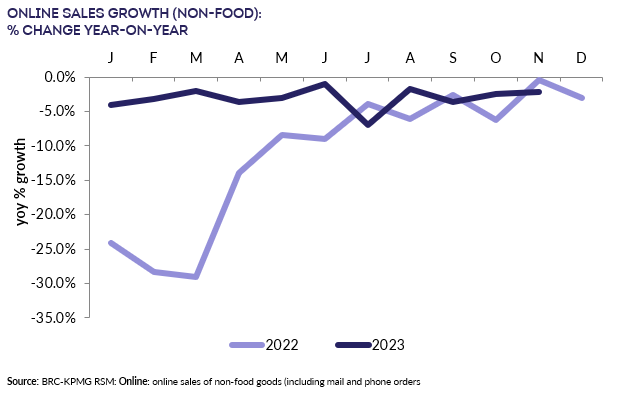

Online Non-Food sales decreased by 2.1% in

November, against a decline of 0.4% in November 2022. This was

shallower than the 3-month decline of 2.8% and deeper than the

12-month decline of 3.0%.

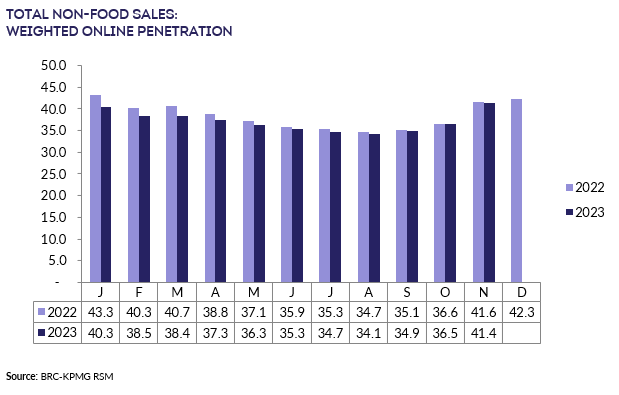

The proportion of Non-Food items bought online (penetration rate)

decreased to 41.4% in November from 41.6% in November 2022.

Helen Dickinson OBE, Chief Executive

of the British Retail Consortium, said:

“Black Friday began earlier this year as many retailers tried to

give sales a much-needed boost in November. While this had the

desired effect initially, the momentum failed to hold throughout

the month, as many households held back on Christmas spending.

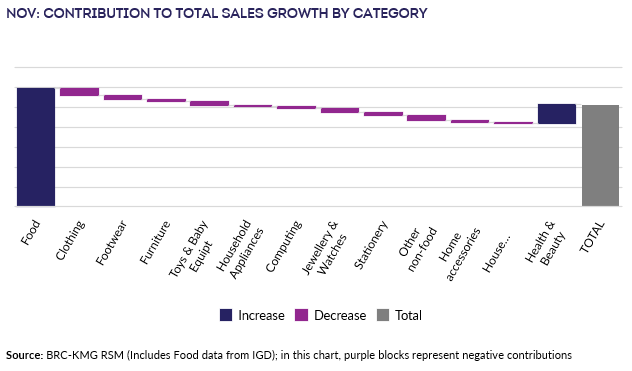

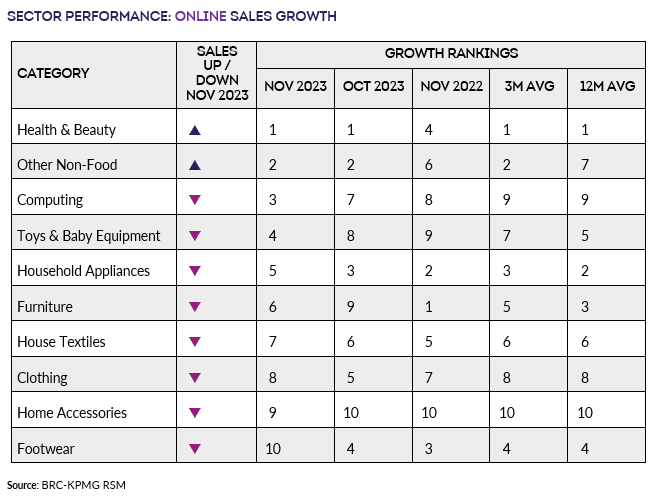

Health and beauty products showed stronger growth, but non-food

sales were down overall year on year. November had the highest

proportion of non-food goods purchased online for 2023, though

this remains below the previous years’ level.

“Retailers are banking on a last-minute flurry of festive

frivolity in December and will continue working hard to deliver

an affordable Christmas for customers so everyone can enjoy some

Christmas cheer. Looking ahead to 2024, retailers will have to

shoulder many new cost pressures, including a rise to business

rates, as well as costs from other new regulations. These

combined with the biggest rise on record to the National Living

Wage will mean retailers will have less capital to invest in

lowering prices for their customers.”

, UK Head of Retail, KPMG,

said:

“With the clock ticking down to Christmas, sales growth in

November remained weak at 2.7%, despite a big push from retailers

around Black Friday deals.

“Food and drink, health, personal care and beauty categories

continued to drive growth whilst jewellery and watches saw the

biggest decline in sales on the high street, suggesting consumers

are abandoning expensive presents in favour of more budget

friendly gifting. Online sales fell yet again, but

penetration rates rose by 5% on October to 41.5% as consumers

shopped around for Black Friday bargains.

“With less than a month to go and sales growth limping along, the

cost-of-living crisis has taken its toll on Christmas spending

for many households, and the continued economic conditions are

testing consumer resilience. Price remains the main

purchasing driver, so we are likely to see a prolonged and well

targeted period of discounting as retailers compete hard for a

shrinking pool of spend and will need to clear stock.

“With two of the three months of the crucial golden quarter

seeing sales growth below 3%, it has already been a weak

Christmas trading period. Any excess stock not sold before

Christmas could be further reduced leading to big January sales,

and potentially having an even greater impact on already tight

margins. As we look to the first few months of 2024, we can

expect the challenges to continue which could lead to further

casualties in the sector, particularly pure online players facing

more than 28 months of consecutive sales decline.”

Food & Drink sector performance | Sarah Bradbury,

CEO, IGD, said:

“For a second month in a row, food and drink sales were down in

November compared to October. The comparatives to November ’22

paint a slightly better picture with an increase in sales,

although this was offset by a marginal decline in volume.

Footfall for the month was down compared to November ’22, a

likely result of storms Ciarán and Debi bringing wetter and more

windy weather across the country.

“IGD’s Shopper Confidence Index enjoyed a slight rise in

November, driven primarily by a rise in confidence among the

lowest income earners. This group were likely boosted by plans

for the national minimum wage to rise announced by the government

in the Autumn Statement. Although lower income earners still

expect to be ‘about the same’ financially next year, rather than

actively better off. Trust in the industry rose again, with 30%

now trusting the food and consumer goods industry to keep prices

low, compared to 24% in October ’23. This is likely to continue

further if general sentiment continues to improve.”