Sales figures are not adjusted for inflation. Given that both the

October SPI (BRC) and September CPI (ONS) show inflation running

at above normal levels, a portion of the sales growth will be a

reflection of rising prices rather than increased volumes.

Covering the four weeks 1 – 28 October

2023

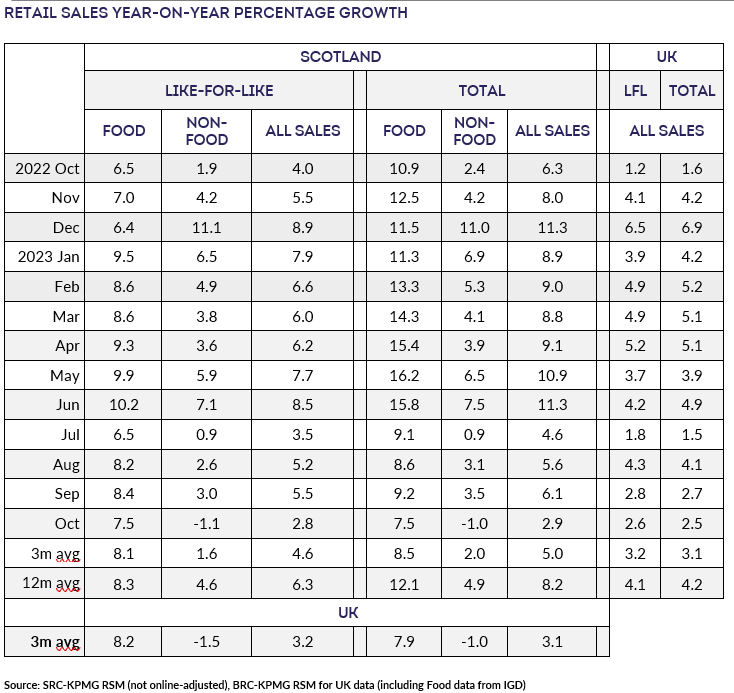

- Total sales in Scotland increased by 2.9% compared with

October 2022, when they had grown 6.3%. This was below the

3-month average increase of 5.0% and below the 12-month average

growth of 8.2%. Adjusted for inflation, the year-on-year decline

was 2.3%.

- Scottish sales increased by 2.8% on a Like-for-like basis

compared with October 2022, when they had increased by 4.0%. This

is below the 3-month average increase of 4.6% and the 12-month

average growth of 6.3%.

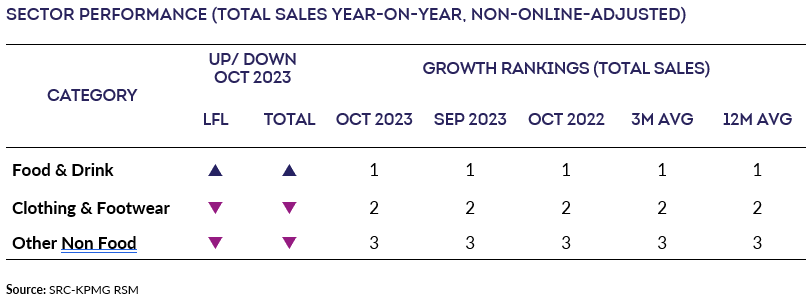

- Total Food sales increased by 7.5% versus October 2022, when

they had increased by 10.9%. October was below the 3-month

average growth of 8.5% and the 12-month average growth of 12.1%.

The 3-month average was below the UK level of 7.9%.

- Total Non-Food sales decreased by 1.0% in October compared

with October 2022, when they had increased by 2.4%. This was

below the 3-month average increase of 2.0% and the 12-month

average of 4.9%.

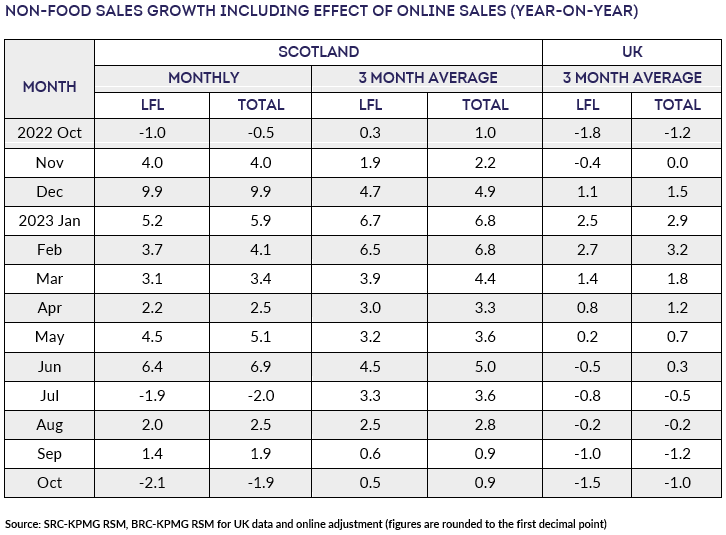

- Adjusted for the estimated effect of Online sales, Total

Non-Food sales decreased by 1.9% in October versus October 2022,

when they had decreased by 0.5%. This is below the 3-month

average growth of 0.9% and the 12-month average of 3.7%.

David Lonsdale, Director | Scottish Retail Consortium

“Severe storms and repeated deluges and disruptions combined with

lingering cost-of-living concerns to put a real dampener on

Scottish retail sales last month. It was a miserable start to

retail’s golden quarter. The significant weakening was the

poorest monthly performance since July and a fourth consecutive

month of real terms decline in the value of retail sales.

“The downturn was seen across all categories but was particularly

pronounced in non-food, which saw its first decline since May.

The growth in grocery sales continued to reduce, mirroring the

fall in food price inflation. Lower-priced indulgencies such as

cosmetics and fragrances fared well, as did sales of Wellington

boots and cold and flu remedies perhaps unsurprisingly given the

drookit conditions. Formalwear was a bright spot as people

returned to corporate events and prepared for the looming party

season, but clothing overall suffered as did sales of larger

ticket items including white goods, electricals, and furniture.

“Hopefully, the downturn in sales is only temporary. That said,

it may continue for a little while yet as indications are that

households are delaying Christmas-related spending in the hope of

grabbing a bargain during Black Friday discounting. With

consumers so price-sensitive it is critical that the Chancellor

and Finance Secretary in their upcoming Budgets seek to support

consumer confidence whilst helping retailers to keep down prices

at the tills. The marked deceleration in shop price inflation

should assist, as should the temporary discounts to peak rail

fares and mooted council tax freeze. However, we need to see

Ministers rule out a hike in the business rate which would add

significantly to shopkeepers’ outgoings and put upward pressure

on prices for consumers.”

, Partner, UK Head of

Retail | KPMG

“Retail sales remained weak in October with growth of just 2.9%

in Scotland, although food and drink and some health and beauty

categories continued to drive sales. Online sales continued to

struggle compared to the same period last year, which could

herald the most competitive Black Friday period that we’ve seen

in a while.

"Despite a decrease in inflation compared to last October's peak

of over 11%, the past 12 months have impacted consumer confidence

and spending ability. With higher interest rates, diminished

COVID savings, and increased heating costs, consumers are now

cautious about their expenditures. This has led to a decline in

the strong demand that sustained some retailers over the past 18

months.

“The upcoming Christmas season poses challenges for retailers as

they compete for a shrinking share of consumer spending through

promotions, further squeezing already tight margins. Anticipated

lower spending levels make this Christmas season potentially the

most challenging since before the pandemic."