BRC-KPMG RETAIL SALES MONITOR – OCTOBER 2023

Sales figures are not adjusted for inflation. Given that both the

October SPI (BRC) and September CPI (ONS) show inflation running

at higher than normal levels, the rise in sales masked a likely

drop in volumes once inflation is accounted for. Like-for-like

data has been moved from the bullets to the tables at the bottom.

Covering the four weeks 1 – 28 October

2023

-

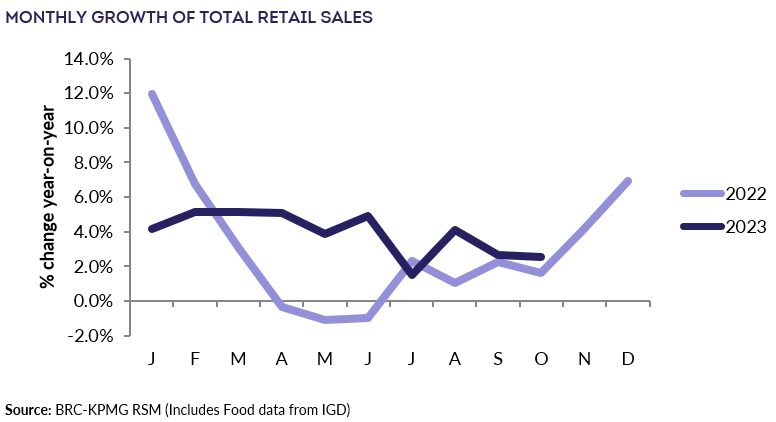

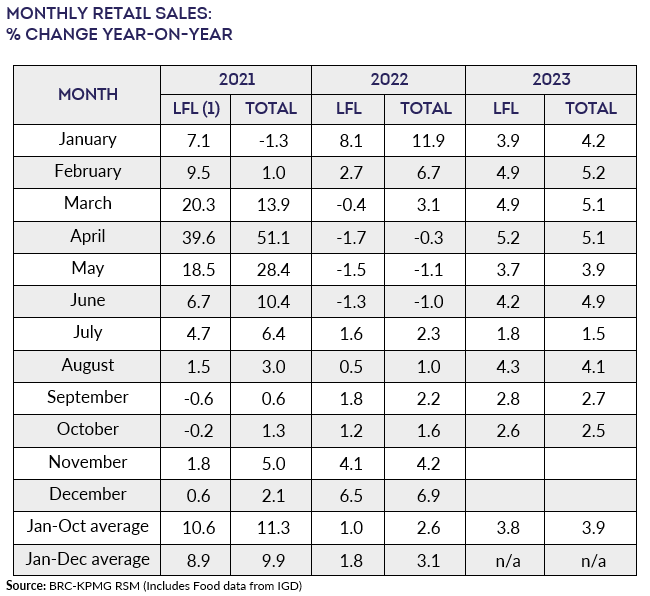

UK Total

retail sales increased by

2.5% in October, against a growth of 1.6% in October 2022. This

was below the 3-month average growth of 3.1% and the 12-month

average growth of 4.2%.

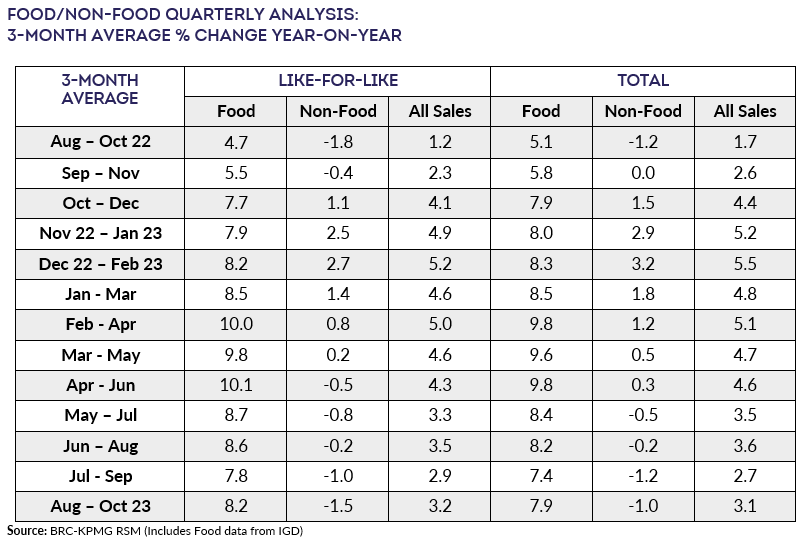

-

Food sales increased 7.9% on a Total

basis over the three months to October. This is below the

12-month average growth of 8.5%. For the month of October, Food

was in growth year-on-year.

-

Non-Food sales decreased 1.0% on a Total

basis over the three-months to October. This is below the

12-month average growth of 0.6%. For the month of October,

Non-Food was in decline year-on-year.

- Over the three months to October, In-store

Non-Food sales decreased 0.1% on a Total basis

since October 2022. This is below the 12-month average growth of

3.0%.

-

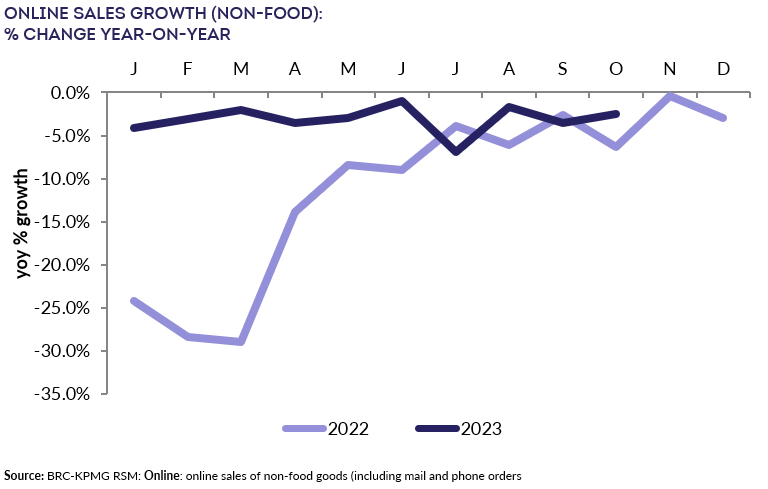

Online Non-Food sales decreased by 2.5%

in October, against a decline of 6.3% in October 2022. This was

shallower than the 3-month decline of 2.7% and deeper than the

12-month decline of 2.9%.

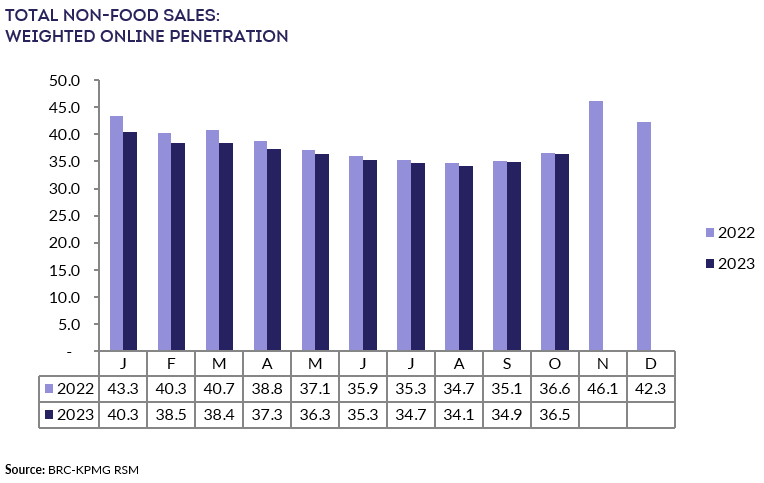

- The proportion of Non-Food items bought online (penetration

rate) decreased to 36.5% in October from 36.6% in October 2022.

Helen Dickinson OBE, Chief Executive

of the British Retail Consortium, said:

“Retail sales growth slowed as high mortgage and rental costs

further shook consumer confidence. Many households are also

delaying their Christmas spending in the hopes they can grab a

bargain in the upcoming Black Friday sales. The cost-of-living

squeeze meant more was spent on lower-price indulgences, such as

beauty products – the so-called ‘Lipstick Effect’. Meanwhile, the

arrival of some colder weather helped to boost fashion sales,

particularly for outdoor wear.

“Retailers continue to invest in lowering prices and streamlining

their operations, part of their commitment to delivering an

affordable Christmas for their customers. But this is put at risk

by the £470m-per-year rise in business rates facing retailers

next year. The Chancellor must freeze rates in the upcoming

Autumn Statement, to prevent extra cost pressure, pushing up

prices for struggling consumers.”

, UK Head of Retail, KPMG,

said:

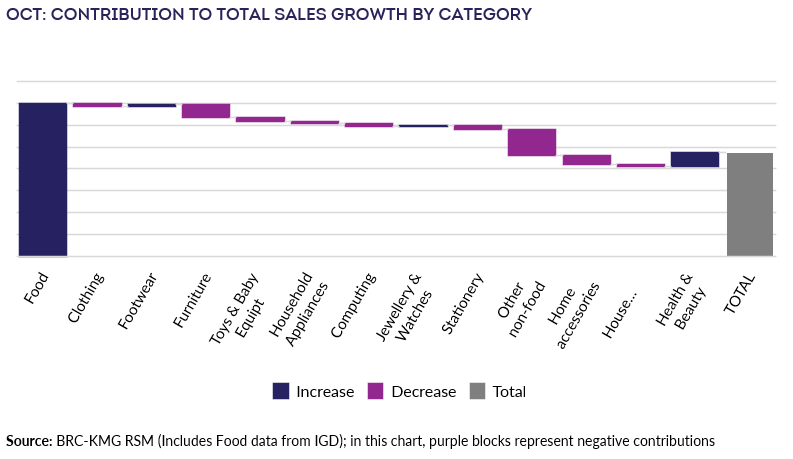

“Retail sales remained weak in October with growth of just 2.5%.

Food and drink and health and beauty categories continued to

drive sales, while a mild October saw consumers put off shopping

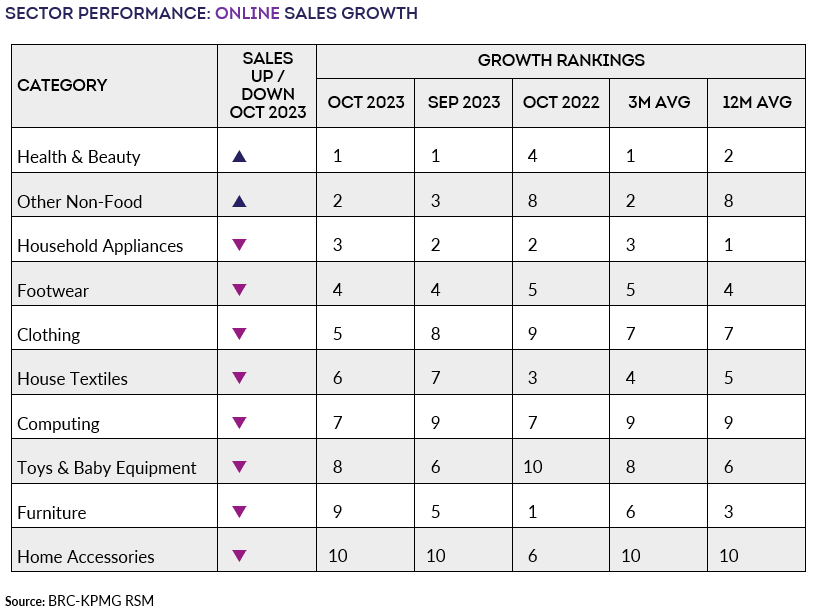

trips to replenish winter wardrobes. Online sales continued

to struggle, with negative sales growth recorded in every

category other than health and Other Non-Food. This could herald

the most competitive Black Friday period that we’ve seen in a

while.

“Whilst consumers are now operating in a lower inflationary

environment compared to October last year where inflation peaked

at over 11%, there is no doubt that the last 12 months have taken

a toll on confidence and their ability to spend. Coupled with a

higher interest rate environment, dwindling covid savings and the

heating coming back on, beleaguered consumers are thinking very

carefully about how they spend their money. As a result,

the strong demand that has kept some retailers afloat over the

last 18 months is now falling away.

“Although the retail sector has done some sterling work around

controlling their own cost environment, the health of the

industry is at the mercy of macro demand. Retailers are facing a

challenging Christmas, competing for a shrinking share of wallet,

driven by promotions that will no doubt cut into already

stretched margins. With spending levels expected to be much

more muted this year, the run up to Christmas could be the most

challenging we’ve seen since pre-pandemic days.”

Food & Drink sector performance | Sarah Bradbury,

CEO, IGD, said:

“October’s food and drink sales enjoyed a slight increase in

volume and value sales compared to last year, but value sales

were slightly down on September’s performance. As the country

enjoyed warm weather at the start of the month the market

benefitted with a slight increase in footfall. Further good news

came as inflation continued to fall against the steep increases

seen a year ago, with shoppers benefitting from reduced prices,

particularly from discounts offered by retailer’s loyalty

schemes.

“Shopper confidence remained the same in October as September and

continues to be at its highest level since December 2021. As

inflation fell again, more shoppers expect food prices to fall in

the year ahead – up to 12%, compared with 8% last month and 3% in

October ‘22. However, some 67% expect prices to rise in the year

ahead and IGD’s food price inflation forecast is for prices to

rise, albeit at a slower rate, indicating there are still

challenges ahead for the industry.”