Fieldwork conducted on 7 - 10 April

2026

According to BRC-Opinium data, consumer expectations

over the next three months of:

-

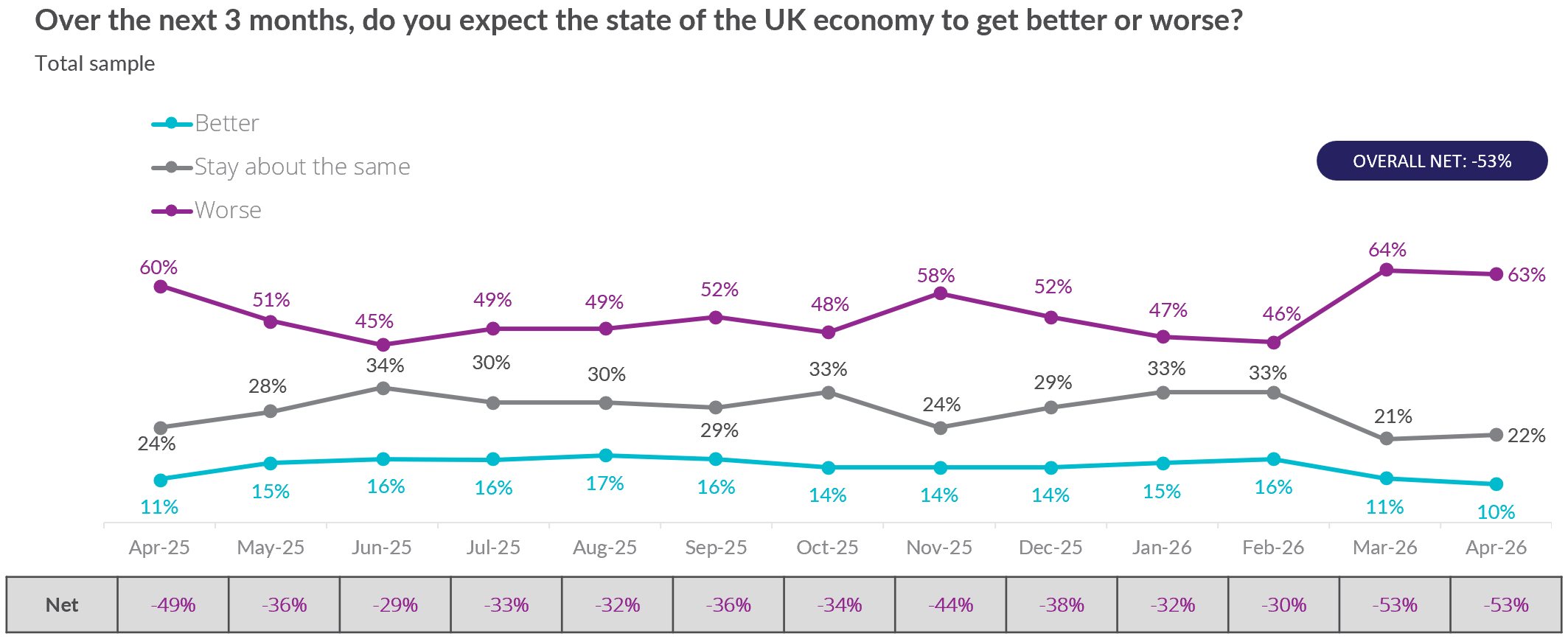

The state of the economy remained at -53 in

April, the same as in March. This remains the lowest on

record.

-

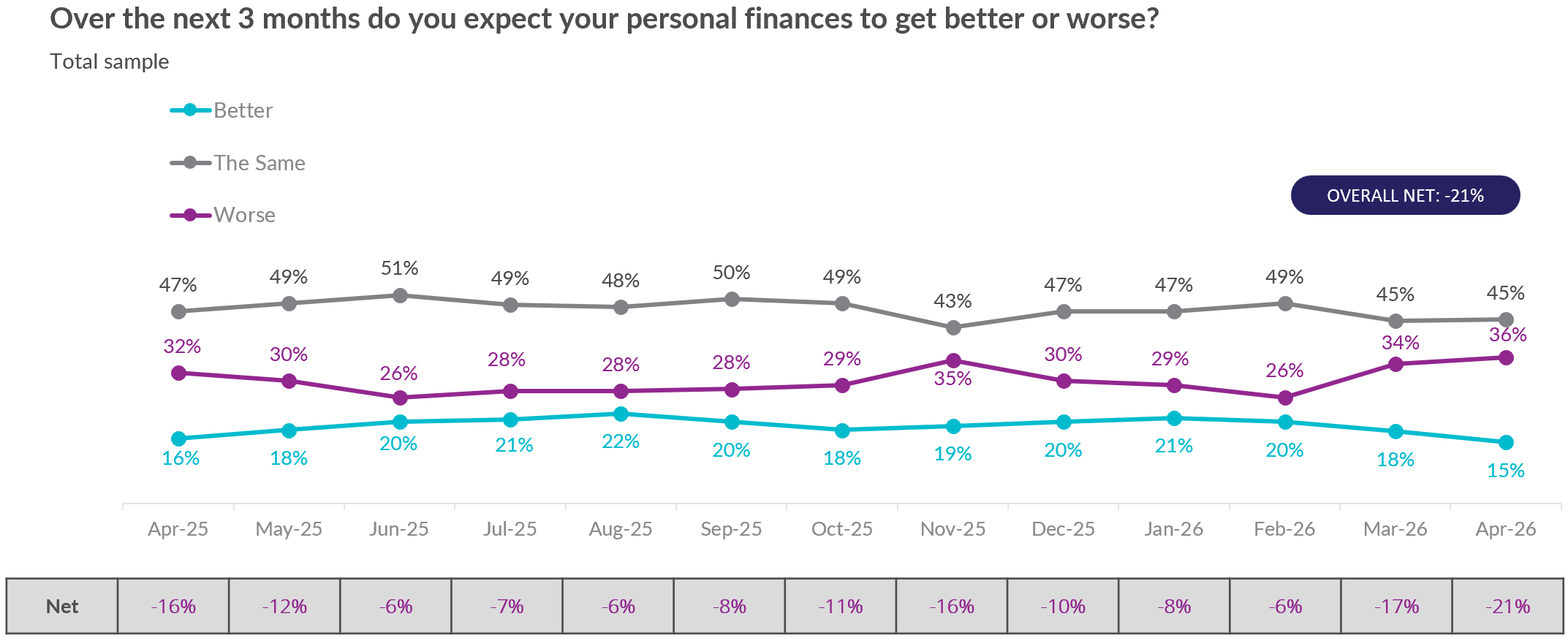

Their personal financial situation worsened to

-21 in April, down from -17 in March. This is the lowest on

record.

-

Their personal spending on retail rose to +5

in April, up from +2 in March.

-

Their personal spending overall rose to +15 in

April, up from +13 in March.

-

Their personal saving remained at -8 in April,

the same as in March.

Helen Dickinson, Chief Executive of the British Retail

Consortium, said:

“The Middle East conflict continues to stoke consumer anxiety

around inflation and the cost of living. Amid a volatile

geopolitical situation, households are expecting to see their pay

packets squeezed by rising petrol, domestic energy, and food

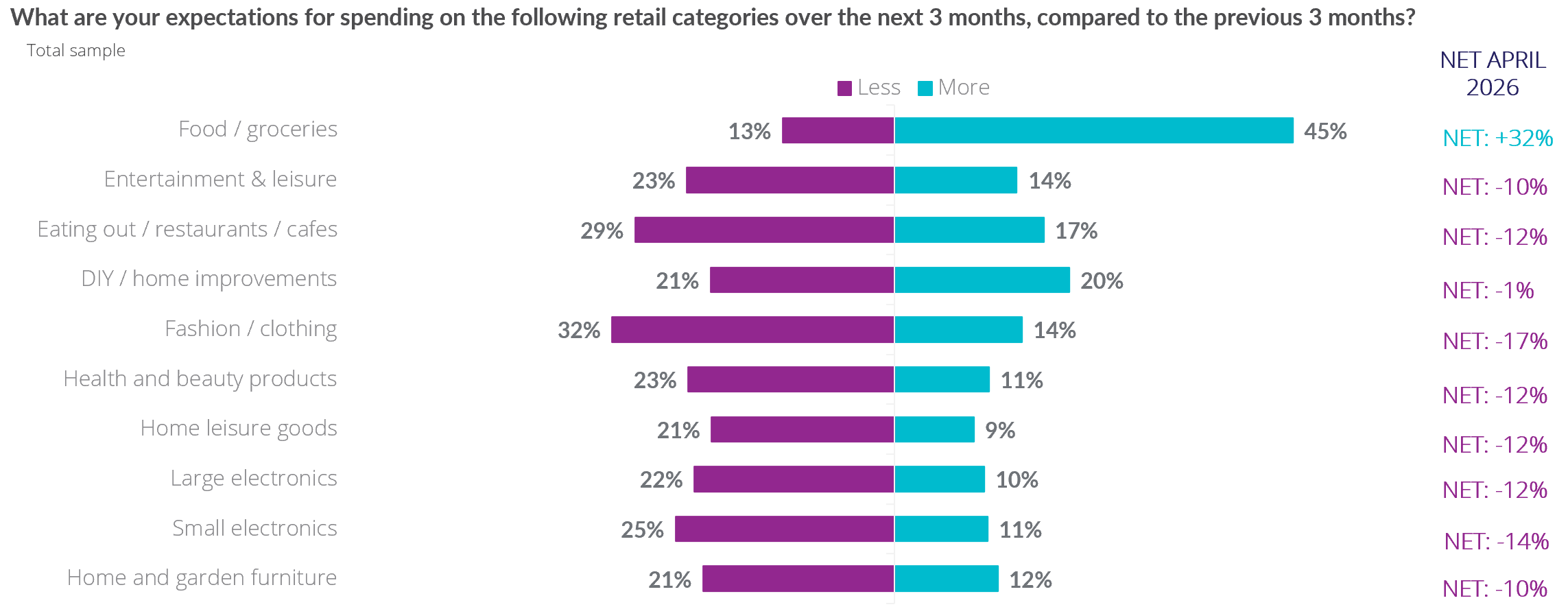

prices. Expected retail spending rose, but this was driven

entirely by grocery spend, with most consumers expecting to rein

in spending in other areas.

“The longer volatility drags on, the more uncertainty it creates

in the economy. Businesses are battered by higher energy costs

while also grappling with the growing burden of domestic policy

pressures. From new packaging taxes to incoming employment and

health regulations, the government has levers it can pull to

limit the inflationary fallout. Taking early, decisive action

would help shield consumers from a spike in the cost of living

they simply can't afford.”

Consumer expectations for the state of the economy

over the next three months:

Consumer expectations for their personal financial

situation over the next three months:

Consumer expectations of spending over the next three

months by category:

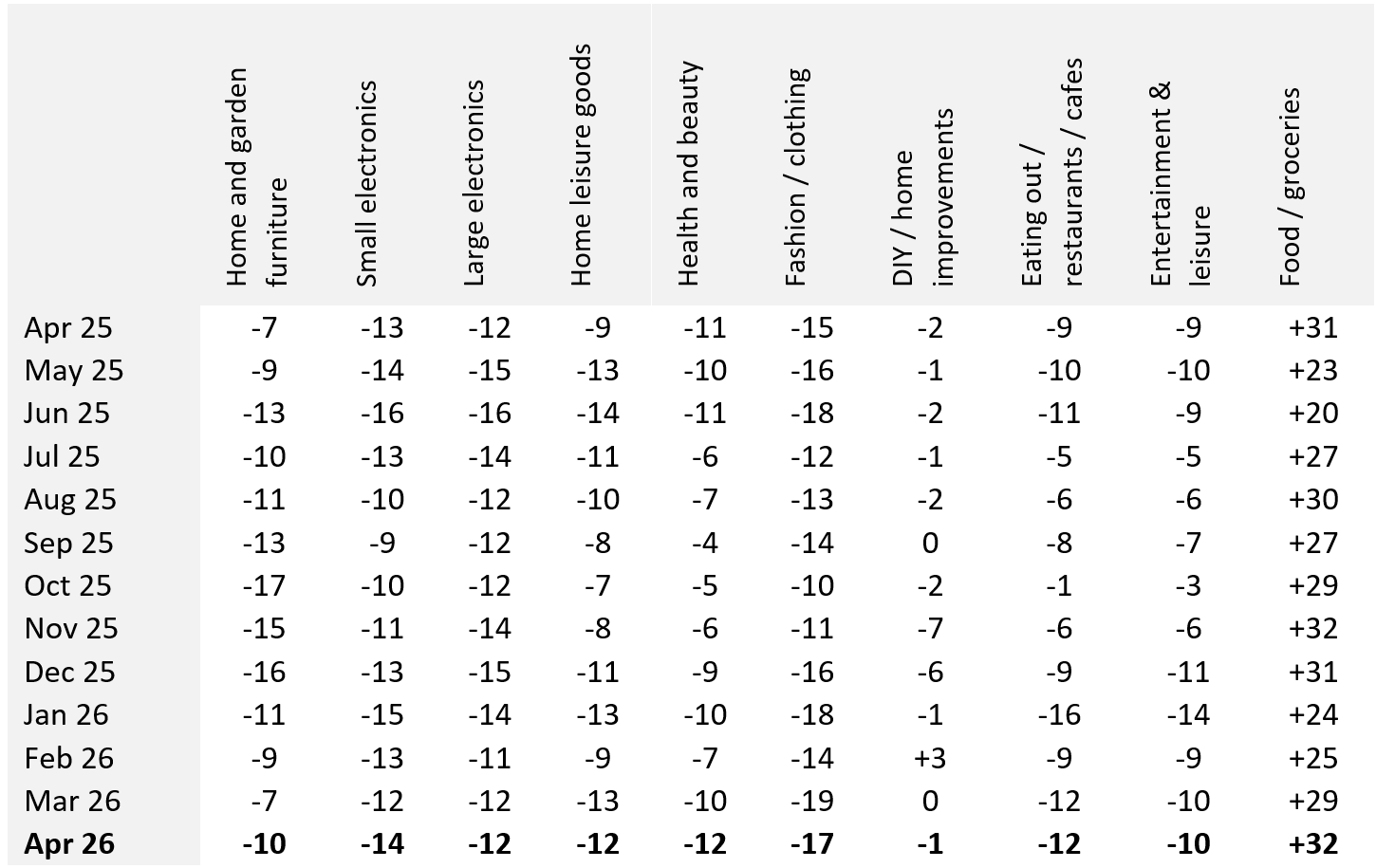

Consumer NET expectations of spending over the next

three months by category:

-ENDS-

Data collection began in March 2024 – and all records are since

then.

The BRC sent this release to our "Monitors" and "General

Retail" media list. To check/update what media lists you are on,

please contact us below.

Methodology:

Fieldwork conducted by Opinium for the BRC. Sample included 2,000

UK adults and results have been weighted and assigned a net

score. The better/worse figures in the graphs are rounded, while

net scores are calculated from precise figures. Questions were:

- Over the next 3 months, do you expect your personal finances

to get better or worse?

- Over the next 3 months, do you expect the state of the UK

economy to get better or worse?

- What do you plan to do in relation to your spending over the

next 3 months?

- Reflecting on your retail spend across different categories,

overall do you expect to spend more or less on retail items over

the next 3 months?

- What are your expectations for saving over the next 3 months?

- What are your expectations for spending on the following

retail categories over the next three months compared to the

previous 3 months?

If you would like the results of the questions by Gender,

Generation, Location, Working status, or Income, please contact

the Press Office. Generations are defined as: Gen Z (18-29),

Millennial (30-45), Gen X (46-61), Boomer (62-80) and Silent

Generation (81+).

This monitor was started in March 2024, and records are from this

date.