Covering the 5 weeks of 1 March – 4 April 2026

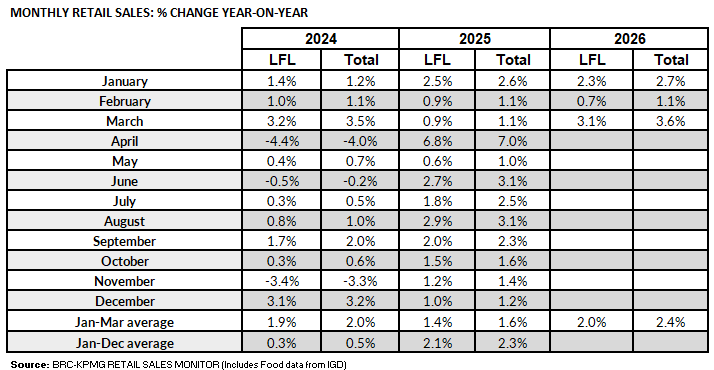

- UK Total retail sales increased by 3.6% year on year in

March, against a growth of 1.1% in March 2025. This was above the

12-month average growth of 2.6%.

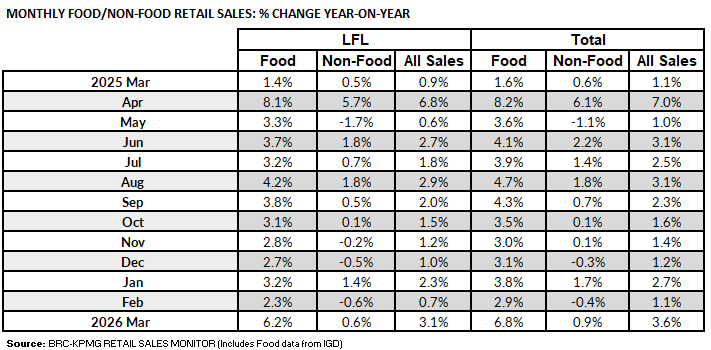

- Food sales increased by 6.8% year on year in March, against a

growth of 1.6% in March 2025. This was above the 12-month average

growth of 4.3%.

- Non-Food sales increased by 0.9% year on year in March,

against a growth of 0.6% in March 2025. This was below the

12-month average growth of 1.1%.

- In-Store Non-Food sales increased by 1.4% year on year in

March, against a decline of 0.1% in March 2025. This was above

the 12-month average growth of 1.1%.

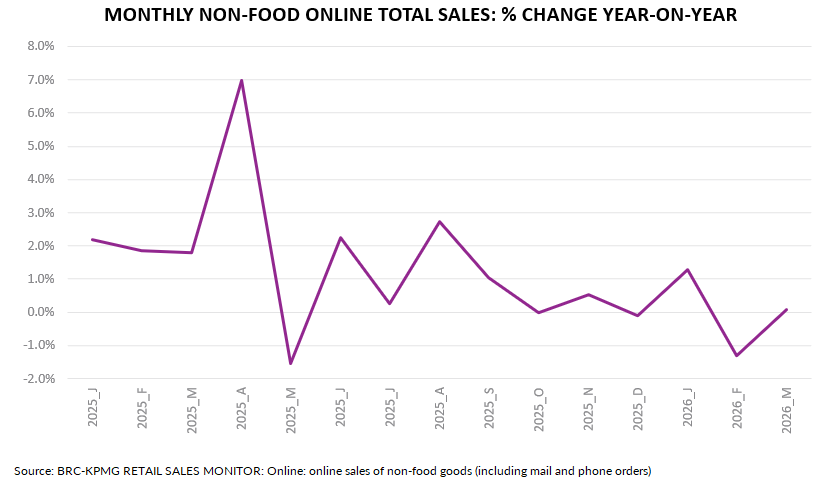

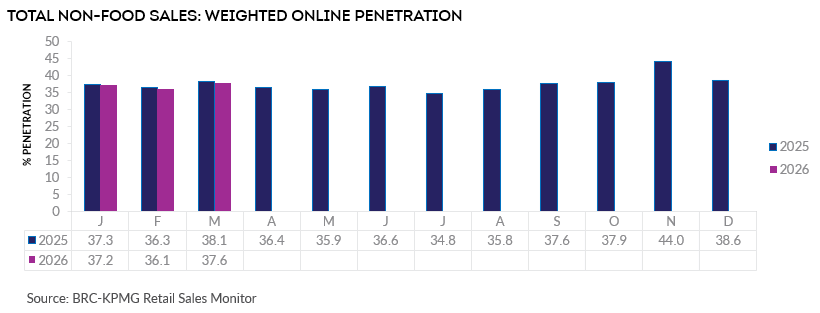

- Online Non-Food sales increased by 0.1% year on year in

March, against a growth of 1.8% in March 2025. This was below the

12-month average growth of 1.0%.

- The online penetration rate (the proportion of Non-Food items

bought online) decreased to 37.6% in March from 38.1% in March

2025. This was above the 12-month average of 37.4%.

Helen Dickinson, Chief Executive at the British Retail

Consortium, said:

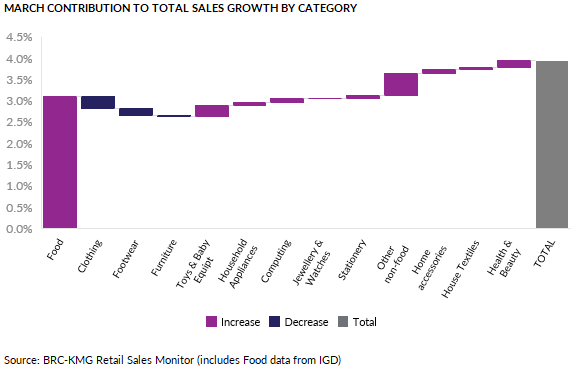

“An early Easter provided a much-needed boost to food sales as

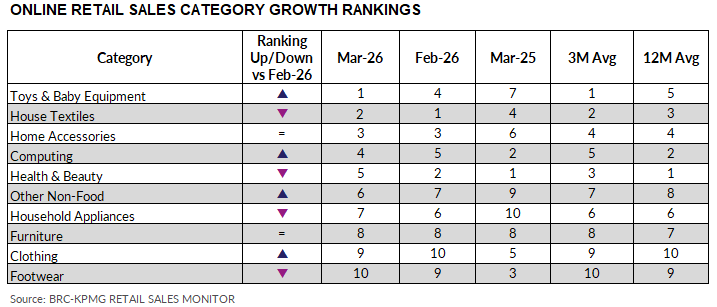

families came together over the long weekend. Non-food

performance was more uneven: demand was robust for computers,

toys, and homeware, but clothing and footwear continued to

struggle. The disruption to international travel caused by the

Middle East conflict also hit sales of travel-related goods.

“Retailers hope that the Middle East ceasefire will bring lasting

stability, but the outlook remains uncertain. Damage to supply

chains has already been done, and rising costs - from shipping

and fertiliser to insurance and commodities - are piling yet more

pressure onto already stretched retailers. Government must act

decisively and boldly now to curb inflation by delaying domestic

policies that would push prices even higher for shoppers.”

Linda Ellett, UK Head of Consumer, Retail & Leisure,

KPMG, said:

“Food and drink continue to drive monthly retail sales growth,

with inflation a key factor. Non-food sales growth remains

tepid, growing at under 1% so far this year, as consumer spending

caution is heightened by the current and potential impact of the

Middle East conflict.

“Despite this challenging trading landscape, monthly examples of

category sales growth remain, with mobile phone and computing,

beauty products and toys and baby goods all up in March.

While margins remain under pressure on a number of fronts,

retailers need to continue to focus on their month-to-month

pricing and promotions, their supply chain resilience and

delivering the technological transformation needed to set the

foundations for growth.”

Food & Drink sector performance | Sarah Bradbury,

CEO, IGD, said:

“The conflict in the Middle East is having an immediate impact on

costs with petrol prices up by around 18% at the pump compared to

before the conflict began. Expectations are that the conflict

will continue to increase cost pressures, with rising risks to

heating bills, food prices and interest rates. As a result,

shopper confidence has dropped to the lowest level since 2023.

While occasions such as Mother's Day and Eid provided moments of

celebration, they were not enough to offset growing shopper

concerns about rising costs. The months ahead will therefore be

challenging for both shoppers and the food and drink industry.”