BRC-KPMG RETAIL SALES MONITOR – JULY

2025

Covering the four weeks 06 July to 02 August 2025

-

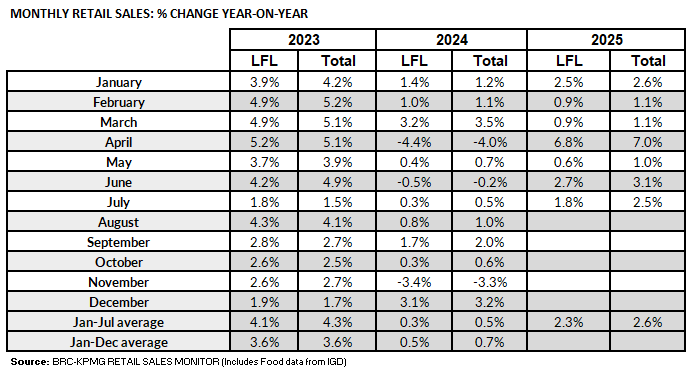

UK Total retail sales increased by 2.5%

year on year in July, against a growth of 0.5% in July 2024.

This was above the 12-month average growth of 1.9%.

-

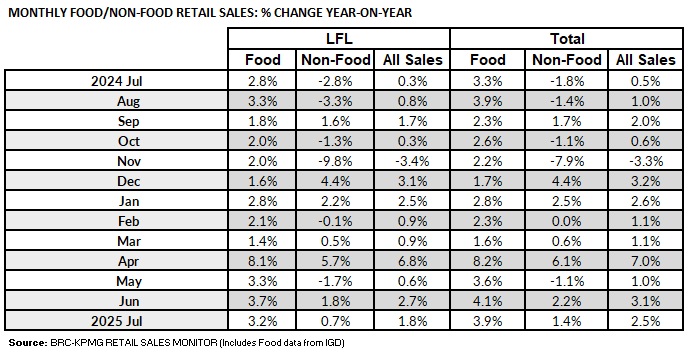

Food sales increased by 3.9% year on year

in July, against a growth of 3.3% in July 2024. This was

above the 12-month average growth of 3.2%.

-

Non-Food sales increased by 1.4% year on

year in July, against a decline of 1.8% in July 2024. This was

above the 12-month average growth of 0.8%.

-

In-Store Non-Food sales increased by 1.9%

year on year in July, against a decline of 3% in July 2024.

This was above the 12-month average growth of 0.2%.

-

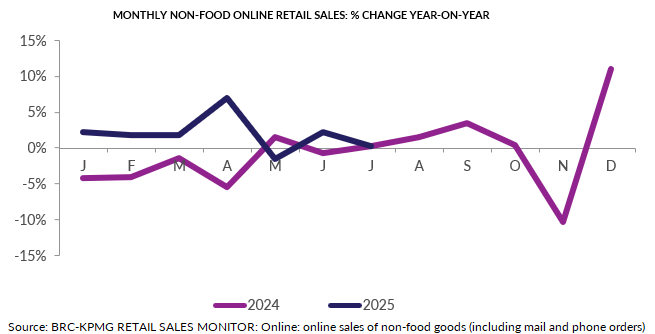

Online Non-Food sales increased by 0.3%

year on year in July, against a growth of 0.3% in July 2024.

This was below the 12-month average growth of 1.9%.

-

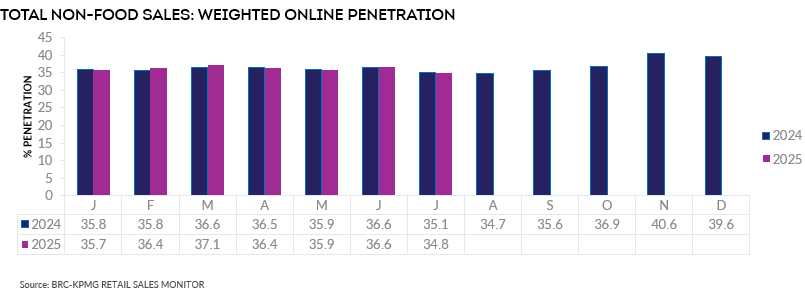

The online penetration rate (the

proportion of Non-Food items bought online) decreased to 34.8%

in July from 35.1% in July 2024. This was below the 12-month

average of 36.7%.

Helen Dickinson, Chief Executive of the British Retail

Consortium, said:

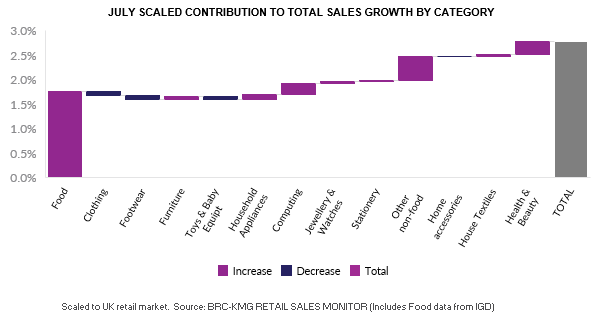

“Food sales did well in early July thanks to warm weather and a

packed sporting schedule, though this momentum failed to hold for

the rest of the month. Rising food inflation meant increased

spending was more a result of higher prices than improved demand.

Fashion sold well early in the month, but deteriorated as weather

worsened, while homeware and indoor furniture grew steadily,

recovering from the previous year's decline. Gaming and toys sold

particularly well, as nostalgic adults purchased products like

Lego.

“With sales growth at these levels, it is barely touching the

sides of covering the £7bn new costs imposed on retailers at the

last Budget. If the upcoming Autumn Budget sees more taxes levied

on retailers' shoulders many will be forced to make difficult

choices about the future of shops and jobs, and ongoing pressure

would push prices higher. Ultimately, this means more families

struggling, particularly those on lower incomes, reduced consumer

spending and a drag on economic growth.”

Linda Ellett, UK Head of Consumer, Retail & Leisure,

KPMG, said:

“The UK's fifth warmest July on Met Office record brought a boost

to home appliance and food and drink sales. But rising

inflation was also a driver of the latter and monthly non-food

sales are only growing at around 1% on average at present.

With employment costs having risen and inflation both a business

and consumer side pressure, it remains a challenging trading

environment for many retailers.

“While the majority of consumers that KPMG surveys are confident

in their ability to balance their monthly household budgets, big

ticket purchases are more considered in the context of rising

essential costs and ongoing caution about the economy and labour

market. Holidays are the priority for many this summer but

those heading away have had to account for a higher cost of

travel. Consequently, spending in some areas of the retail

sector remains subdued and competition for consumer spend will

remain fierce.”

Food & Drink sector performance | Sarah Bradbury,

CEO, IGD, said:

“July's shopper confidence fell to zero for the first time since

April, cooling alongside the weather despite boosts from

Wimbledon and the Lionesses' win. More households are feeling the

pinch yet trust in the industry rose by three points. With food

price inflation climbing to 4.5% and economic uncertainty

growing, shoppers face a tough outlook. Own label products

continue to outperform brands, but modest volume growth shows

inflation is masking any gains. A potential interest rate cut,

and a sunny bank holiday could offer a much-needed boost at the

end of the summer.”