Covering the four weeks 29 September – 27 October

2024

-

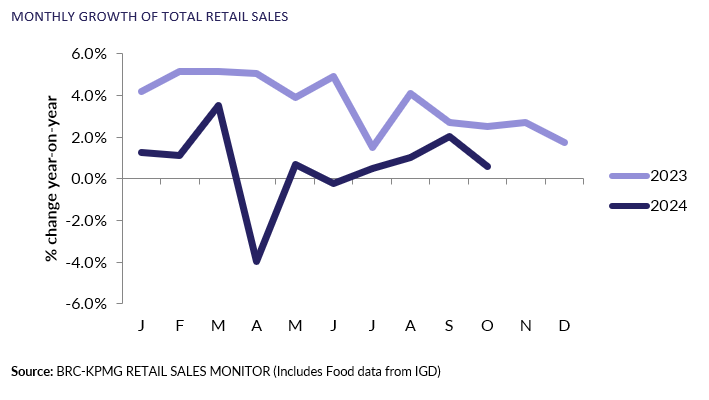

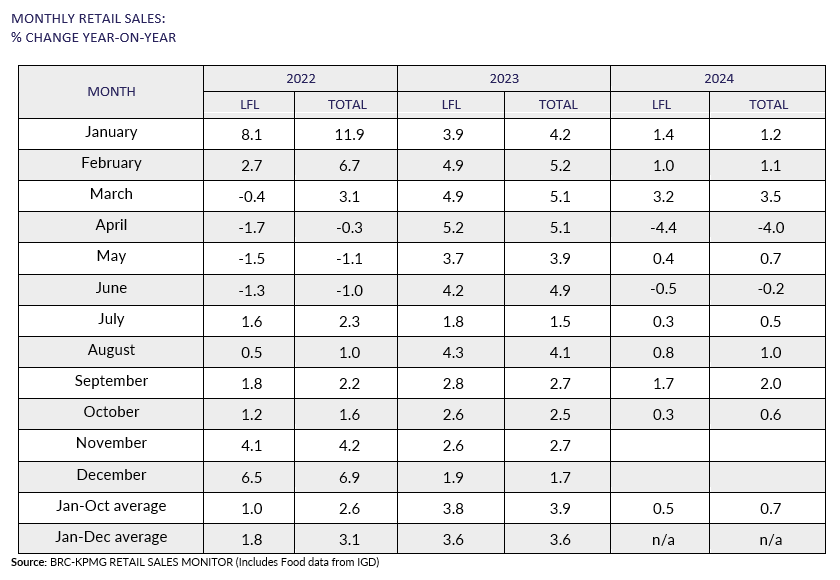

UK Total retail sales

increased by 0.6% year on year in October, against a growth of

2.6% in October 2023. This was below the 3-month average growth

of 1.3% and the 12-month average growth of 1.0%.

-

Food sales increased 2.9% year on year over

the three months to October, against a growth of 7.9% in

October 2023. This is below the 12-month average growth of

4.1%. For the month of Oct, Food was in growth

year-on-year.

-

Non-Food sales decreased 0.1% year on year

over the three-months to October, against a decline of 1.0% in

October 2023. This is above the 12-month average decline of

1.6%. For the month of October, Non-Food was in decline

year-on-year.

-

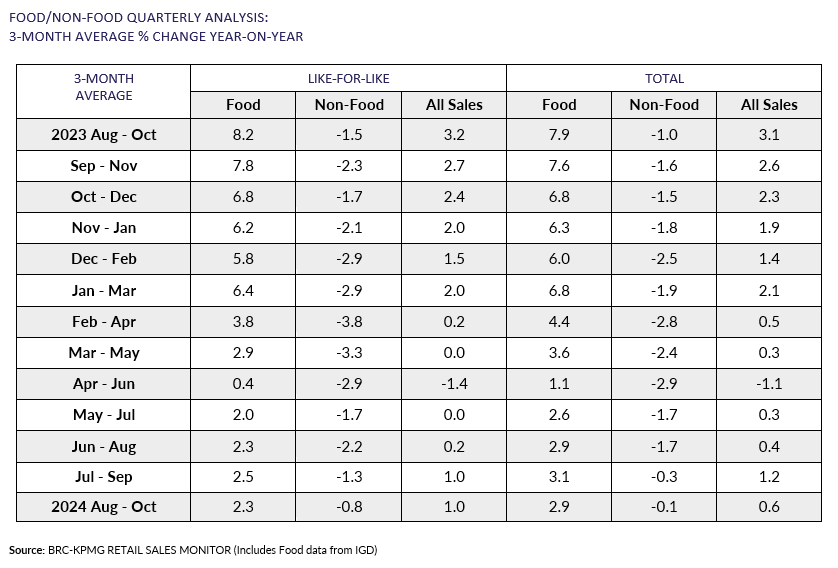

In-store Non-Food sales over the three months

to October decreased 1.2% year on year, against a decrease of

0.1% in October 2023. This is above the 12-month average

decline of 2.0%.

-

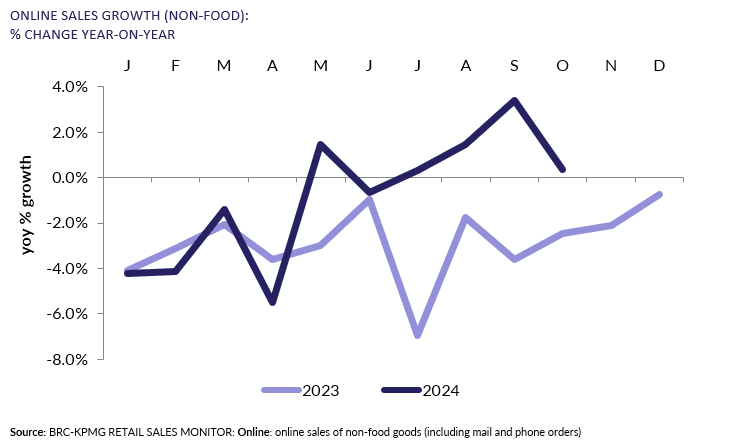

Online Non-Food sales increased by 0.4% year

on year in October, against an average decline of 2.5% in

October 2023. This was below the 3-month average increase of

1.9% and above the 12-month average decline of 0.9%.

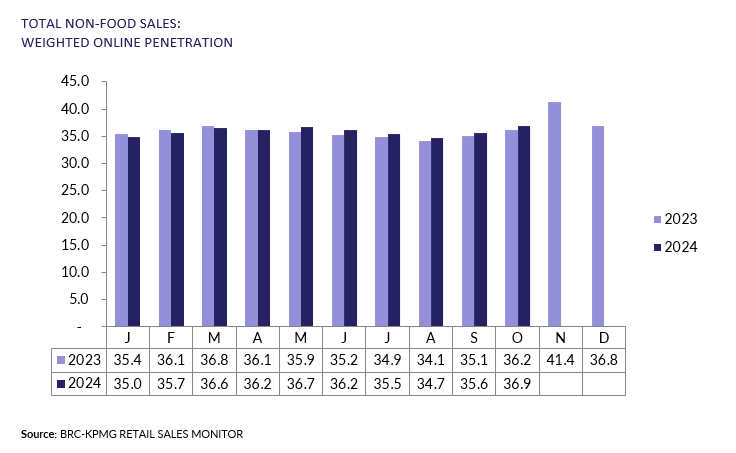

- The online penetration rate (the proportion

of Non-Food items bought online) increased to 36.9% in October

from 36.2% in October 2023. This was below the 12-month average

of 36.4%.

Helen Dickinson OBE, Chief Executive

of the British Retail Consortium, said:

“After a good start to Autumn, October's sales growth was

disappointing. This was part driven by half term falling a week

later this year, depressing the October figures, and November

sales will likely see more of a boost. Uncertainty during the

run-up to the Budget, coupled with rising energy bills, also

spooked some consumers. Fashion sales took the biggest hit as the

mild weather delayed winter purchases. Health and beauty sales

remained buoyant, with beauty advent calendars flying off the

shelves.

“After a painful Budget for retailers, the hope is it will be

less painful for households in the immediate term and consumer

appetite will pick up in time for the Black Friday sales and

festive season. Retailers must now grapple with over £5bn of new

costs announced by the Chancellor, including in Employer National

Insurance, Business Rates and the uplift in the National Living

Wage. Managing this will hold back investment and growth in the

short term, while further squeezing already-low margins and

risking inflation.”

Linda Ellett, UK Head of Consumer, Retail & Leisure,

KPMG, said:

“While October's growth didn't continue at the levels seen for

the retail sector in September, retailers will feel that there is

mitigation and that they can pick up the pace again in November.

"Speculation about the impact of the Budget, a holding back of

demand until Black Friday promotions, and a later half term break

all impacted retail sales data over the last month.

“With clarity now provided by the Budget and many households

escaping paying increased tax from their wages, retailers will be

hoping for an upturn in consumer confidence and spending. Any

positivity from retailers though will of course be dampened given

the increased employment costs that they face.

“The promotional weeks around Black Friday will be the first real

test of post-Budget consumer sentiment, with retailers looking to

electronics promotions and new AI-linked products to build on the

computing and mobile phone sales growth that has been one of the

better areas of sales performance in recent months.”