Sales figures are not adjusted for inflation. Given that both the

May SPI (BRC) and April CPI (ONS) show inflation running at

historically record levels, the rise in sales masked a much

larger drop in volumes once inflation is accounted for.

Covering the four weeks 30 April – 27 May

2023

-

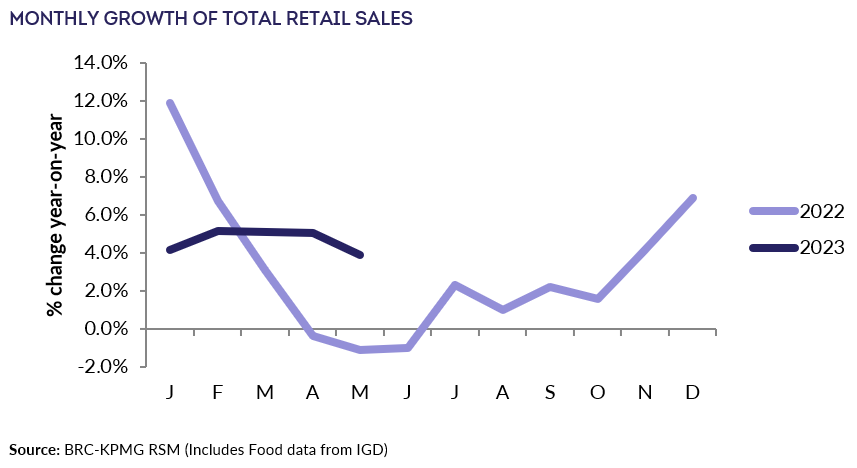

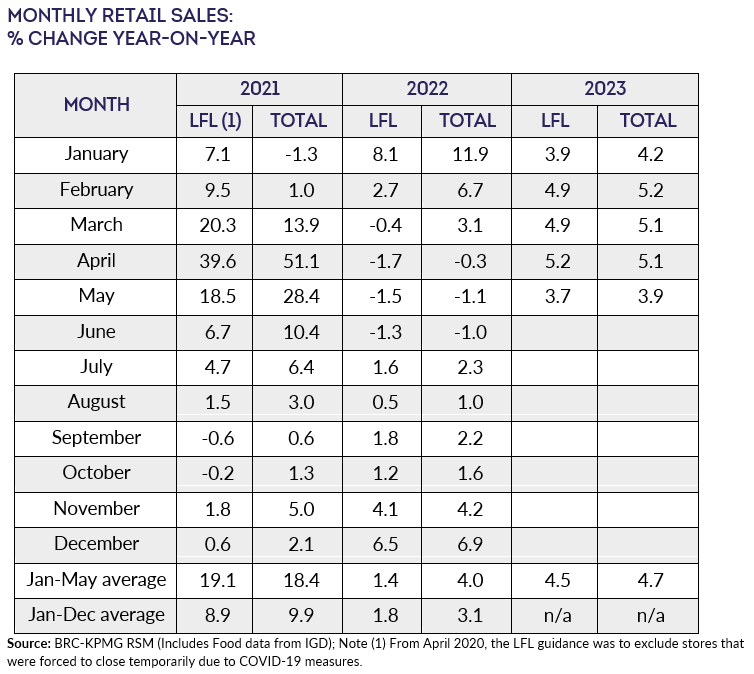

UK Total retail sales

increased by 3.9% in May, against a decline of 1.1% in May

2022. This is below the 3-month average growth of 4.7% and

above the 12-month average growth of 3.4%.

-

UK Like-for-like retail sales increased by

3.7% in May, against a decline of 1.5% in May 2022. This was

below the 3-month average growth of 4.6% and above the 12-month

average growth of 3.1%.

-

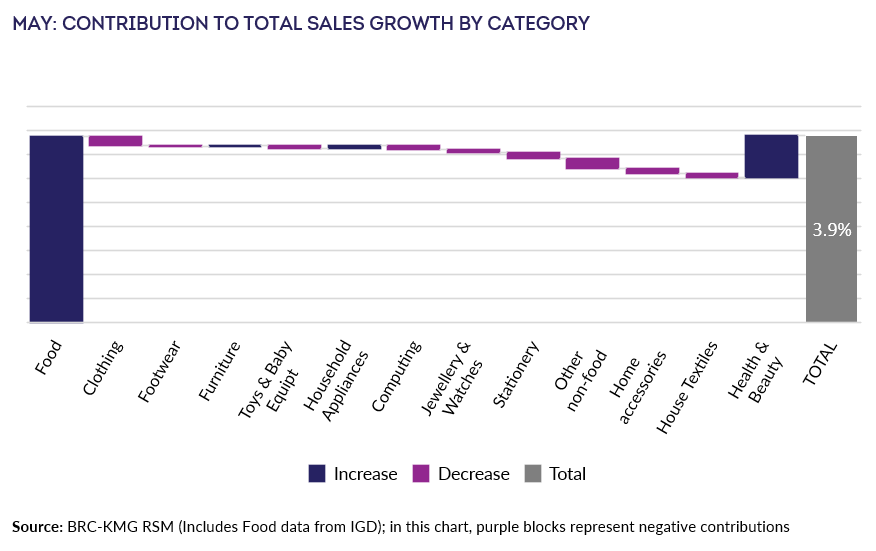

Food sales increased 9.6% on a Total basis and

9.8% on a Like-for-like basis over the three months to May.

This is above the 12-month Total average growth of 6.9%. For

the month of May, Food was in growth year-on-year.

-

Non-Food sales increased 0.7% on a Total basis

and 0.5% on a like-for-like basis over the three-months to May.

This is above the 12-month Total average growth of 0.5%. For

the month of May, Non-Food was in growth year-on-year.

- Over the three months to May, In-store Non-Food

sales increased 2.9% on a Total basis and 2.2% on a

Like-for-like basis since May 2022. This is below the Total

12-month average growth of 3.7%.

-

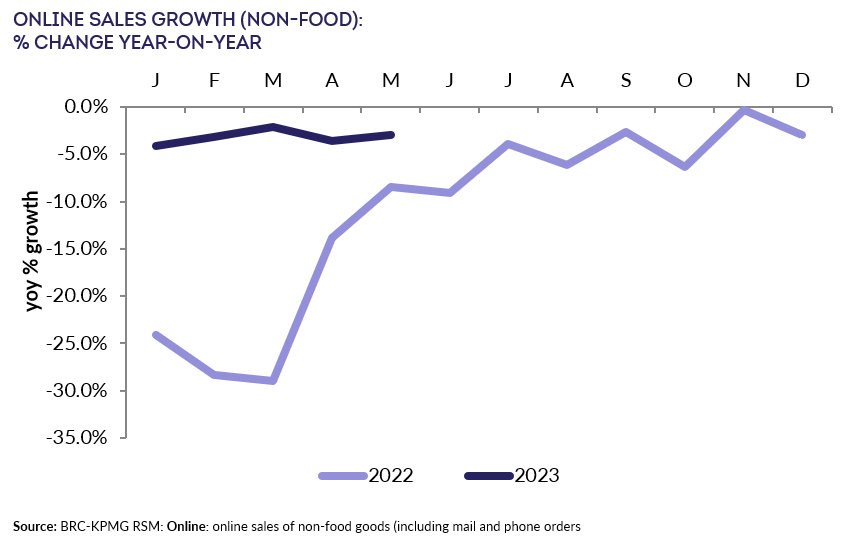

Online Non-Food sales decreased by 3.0% in

May, against a decline of 8.5% in May 2022. This is steeper

than the 3-month average decline of 2.8% and shallower than the

12-month decline of 4.0%.

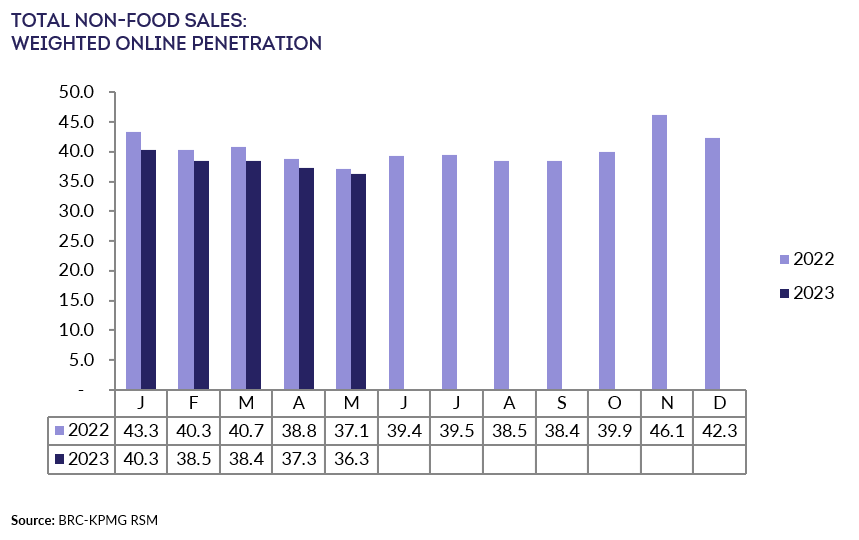

- The proportion of Non-Food items bought online (penetration

rate) decreased to 36.3% in May from 37.1% in May 2022.

Helen Dickinson OBE, Chief Executive | British Retail

Consortium

“The trio of bank holidays failed to get

shoppers spending as sales growth slowed to its lowest level in

six months. While food sales got a boost from the Coronation

weekend, this was not sustained for the rest of the month.

Meanwhile, growth in discretionary spend continued to tumble as

the high cost of living squeezed households. There was cause for

some optimism, however, as brighter weather at the end of the

month led to a much-needed pick-up in summer fashion sales, as

well as gardening and DIY products.

“With consumer confidence still recovering from record depths,

and continued tightening of household incomes, we are unlikely to

see substantial sales growth in the coming months. But, with

signs that inflation has possibly peaked, retailers are hopeful

that confidence will continue to improve. Now is not the time for

Government to impose more regulation and tax on business that

will push up costs for retailers and prices for their customers.”

, UK Head of Retail |

KPMG

“Despite warmer weather, a national

celebration and month of bank holidays, retailers saw pretty mild

growth in May with sales figures up just 3.9% on last year, and

lower than the 5% growth seen in April.

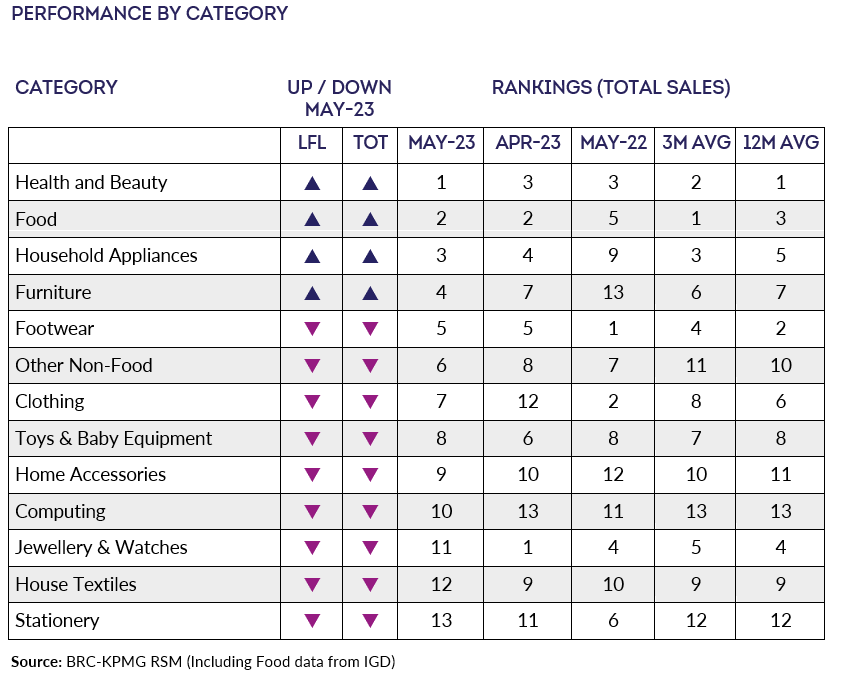

“High street retailers saw more categories slip into negative

sales territory last month, with health, beauty and food driving

sales on the high street. The gloom continued for online

retailers with just four categories registering positive sales

figures and total sales down by 3%. Online penetration

rates continued to slide, sitting at 36%, as consumers return to

bargain hunting in store.

“Retailers will be hoping that inflation levels in the wider

economy continue to move in the right direction in order to boost

much needed consumer confidence. The wild card for the

retail sector remains uncontrollable food inflation, which shows

little sign of coming down in the near future, and this is having

a significant knock-on effect on non-essential spending.

The grocery sector is the fastest growing part of the consumer

wallet at the moment, so consumers are having to spend more of

their money in the one area that is getting disproportionately

more expensive.

“UK consumers are resilient, but with stubbornly high food

inflation continuing and the prospect of further interest rate

rises threatening to impact their ability to spend elsewhere, it

is likely to be a long, hot summer for the retail sector.”

Food & Drink sector performance | Susan Barratt, CEO

| IGD

“May’s food and drink sales again saw strong value growth, with

double-digit inflation driving sales consistently over the

four-week period. Volume sales were marginally negative, even

with a brief uptick from the events surrounding the Coronation of

King Charles.

“Despite food price inflation reaching its highest level for 45

years in the first quarter of 2023, shoppers overall seem

slightly less fearful about how high prices will go. Although

three-quarters (75%) expect food prices to get more expensive in

the year ahead, this is actually the lowest level since July

2021, and IGD’s Shopper Confidence Index continued to improve in

May to reach its highest level in more than two years. At the

same time, the number of shoppers expecting to be better off

financially in the year ahead has risen, up from 14% this time

last year to 18%.”