Teaching is an attractive profession for a range of reasons; as

well as it being interesting, no two days being the same and

it provides the chance to shape young people’s lives.

Teacher’s pensions are also among the best and safest available.

Here’s what you need to know.

What are the current arrangements for teacher’s

pensions?

The Teachers’ Pension Scheme is a ‘defined benefits’ pension

scheme. That means it offers teachers a guaranteed income in

retirement as opposed to a ‘defined contribution’ scheme, where

income is based on the performance of the pension fund.

Teachers in England and Wales pay into the scheme direct from

their salary each month and it is then topped up by their

employer. Teachers based in Scotland have separate pension

agreements.

In return for the money, they put in, teachers receive an

index-linked (this means it increases in line with the cost of

living) government-backed annual pension for retirement. This is

based on their career average earnings.

Is this the case for all teachers?

In 2015, the government introduced reforms to public service

pension schemes, including the Teachers’ Pension Scheme, which

meant some members receiving Transitional Protection, remained in

the final salary scheme, while others entered the career average

scheme.

These changes have since been deemed discriminatory on age

grounds and the legislation to correct this is being rolled out

in two stages.

Part one of the legislation was the closure of the final salary

scheme from 1 April 2022, with all active members now building up

their pension in the career average scheme.

Part two will give eligible members the option to choose between

their final salary and career average pension scheme benefits

between 1 April 2015 and 31 March 22 (the remedy period).

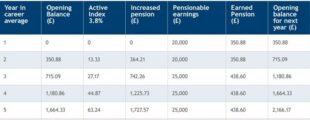

How is the career average pension worked out?

A member will gain a part of their pension for every year they

contribute to the Teachers’ Pension Scheme. This means that a

teacher will add 1/57th to their ‘pot’, depending on

the amount of their earnings and each year that’s increased in

line with indexation. An example of how a career average pension

can grow over five years can be seen below:

How much do teachers and employers contribute?

A teacher’s employer will deduct pension contributions from their

pay before deducting tax, thereby giving tax relief on the

pension contribution. Employers contribute the equivalent of

23.68% of a teacher’s pay towards the cost.

Contribution rates are determined by a teacher’s salary.

|

Annual Salary Rate for the Eligible Employment from 1 April

2022

|

Member Contribution Rate

|

|

Up to £29,187.99

|

7.4%

|

|

£29,188 to £39,290.99

|

8.6%

|

|

£39,291 to £46,586.99

|

9.6%

|

|

£46,587 to £61,742.99

|

10.2%

|

|

£61,743 to £84,193.99

|

11.3%

|

|

£84,194 and above

|

11.7%

|